¡La leyenda en el equipo de InstaSpot!

¡Leyenda! ¿Cree que es una retórica grandilocuente? Pero, ¿cómo deberíamos llamar a un hombre, que se convirtió en el primer asiático en ganar el campeonato mundial de ajedrez júnior a los 18 años y en el primer Gran Maestro indio a los 19 años? Ese fue el comienzo de un camino difícil hacia el título de Campeón del Mundo para Viswanathan Anand, el hombre que se convirtió en parte de la historia del ajedrez para siempre. ¡Ahora una leyenda más en el equipo de InstaSpot!

Borussia es uno de los clubes de fútbol con más títulos en Alemania, que ha demostrado repetidamente a los fanáticos: el espíritu de competencia y liderazgo que ciertamente conducirán al éxito. Opere de la misma manera que los profesionales del deporte: con confianza y de forma activa. ¡Mantenga un "pase" del Borussia FC y lidere con InstaSpot!

The Reserve Bank of New Zealand's quarterly survey of inflation expectations showed a decline from 2.29% to 2.28% over the two-year horizon, providing strong evidence that inflation is stabilizing near the target level. In its July monetary policy review, the RBNZ stated: "If medium-term inflationary pressures continue to ease as projected, the Committee expects further reductions in the Official Cash Rate."

It appears this condition has been met, and analysts at ANZ and BNZ believe that a rate cut to 3% at the 20 August meeting is virtually guaranteed.

BNZ, in particular, expects inflation to be slightly higher in the short term, but sees the medium-term forecast as even weaker than the Bank itself projected. The reasoning is compelling — a significant share of inflation is driven by commodity prices, which have peaked and begun to decline, meaning that over the next two to three months, inflation is also likely to ease. BNZ also reaches another, less obvious conclusion — the kiwi will begin to strengthen as the U.S. economy slows. This assumption is based on the observation that New Zealand's GDP growth could be slightly above forecasts, and overall, the country's economy appears more resilient than that of the United States, where signs of an approaching recession are mounting.

The comparative yield dynamics of 10-year New Zealand government bonds versus U.S. Treasuries have shifted in favor of Treasuries, further indicating that the market is expecting an RBNZ rate cut. There had been concerns that, following the weak U.S. employment report, bond yields would drop sharply due to the threat of a faster Federal Reserve rate-cut cycle. However, that did not happen — the decline was limited, which means only one thing: the market does not expect a change in Fed policy, even if pressure from Donald Trump on the Fed's leadership intensifies significantly.

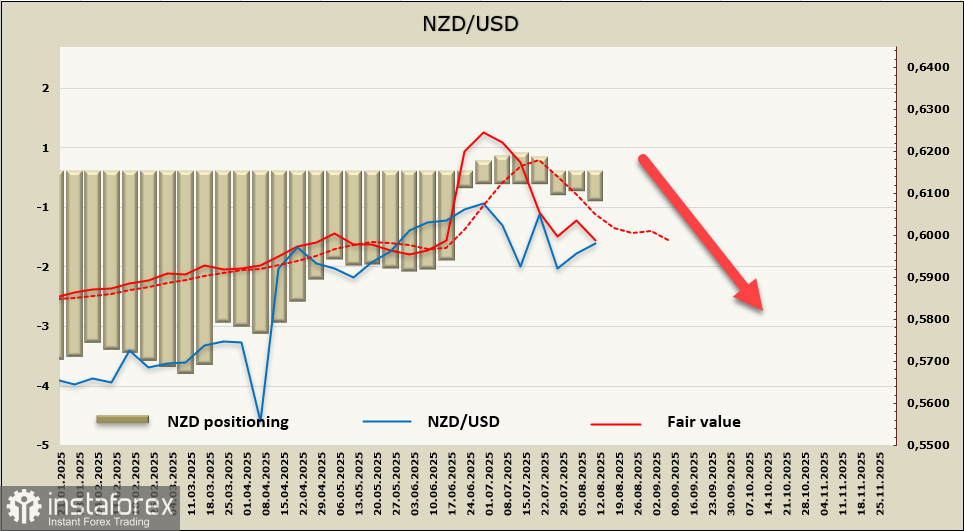

The net short position in the kiwi rose by 161 million to -285 million over the reporting week; given the mild bearish bias, speculative positioning remains neutral. The fair value estimate is trending lower, suggesting continued downside in NZD/USD.

In our previous review, we suggested that trading would shift into a range-bound mode, as equally weak U.S. data offset New Zealand's weak labor market report. Two weaknesses cancel each other out, making it unlikely that the current short-term impulse in the kiwi will extend. We expect NZD/USD to continue falling, with volatility potentially increasing toward the end of the week due to the meeting between the presidents of Russia and the United States, as geopolitical risks will likely be reassessed, which could lead to either a rapid spike in demand for risk assets or a decline in such demand. We expect any attempt to move above 0.6000 to fail, with the kiwi likely to generate another downside impulse targeting 0.5840/50.

*El análisis de mercado publicado aquí tiene la finalidad de incrementar su conocimiento, más no darle instrucciones para realizar una operación.

¡Los informes analíticos de InstaSpot lo mantendrá bien informado de las tendencias del mercado! Al ser un cliente de InstaSpot, se le proporciona una gran cantidad de servicios gratuitos para una operación eficiente.