¡Nuestro equipo cuenta con más de 7,000,000 operadores!

Cada día, trabajamos juntos para mejorar las operaciones. Obtenemos grandes resultados y seguimos adelante.

El reconocimiento de millones de operadores en todo el mundo es el mejor agradecimiento a nuestro trabajo! ¡Usted hizo su elección y haremos todo lo que esté a nuestro alcance para satisfacer sus expectativas!

¡Juntos somos un gran equipo!

InstaSpot. ¡Orgulloso de trabajar para usted!

¡Actor, 6 veces ganador del torneo UFC y un verdadero héroe!

El hombre que se hizo a sí mismo. El hombre que sigue nuestro camino.

El secreto detrás del éxito de Taktarov es el constante movimiento hacia el objetivo.

¡Revele todo los lados de su talento!

Descubra, intente, fracase, ¡pero nunca se rinda!

InstaSpot. ¡Su historia de éxito comienza aquí!

All things come to an end sooner or later. Central banks' experiment with negative rates has come to an end. The Bank of Japan became the last one to abandon them. At its March meeting, it raised the overnight rate from -0.1% to 0%, announced the end of yield curve control, and ceased buying exchange-traded funds as part of its quantitative easing program. However, these events were largely priced in the USD/JPY quotes, which, combined with signals of maintaining an ultra-loose monetary policy, pushed the pair's quotes above 150.

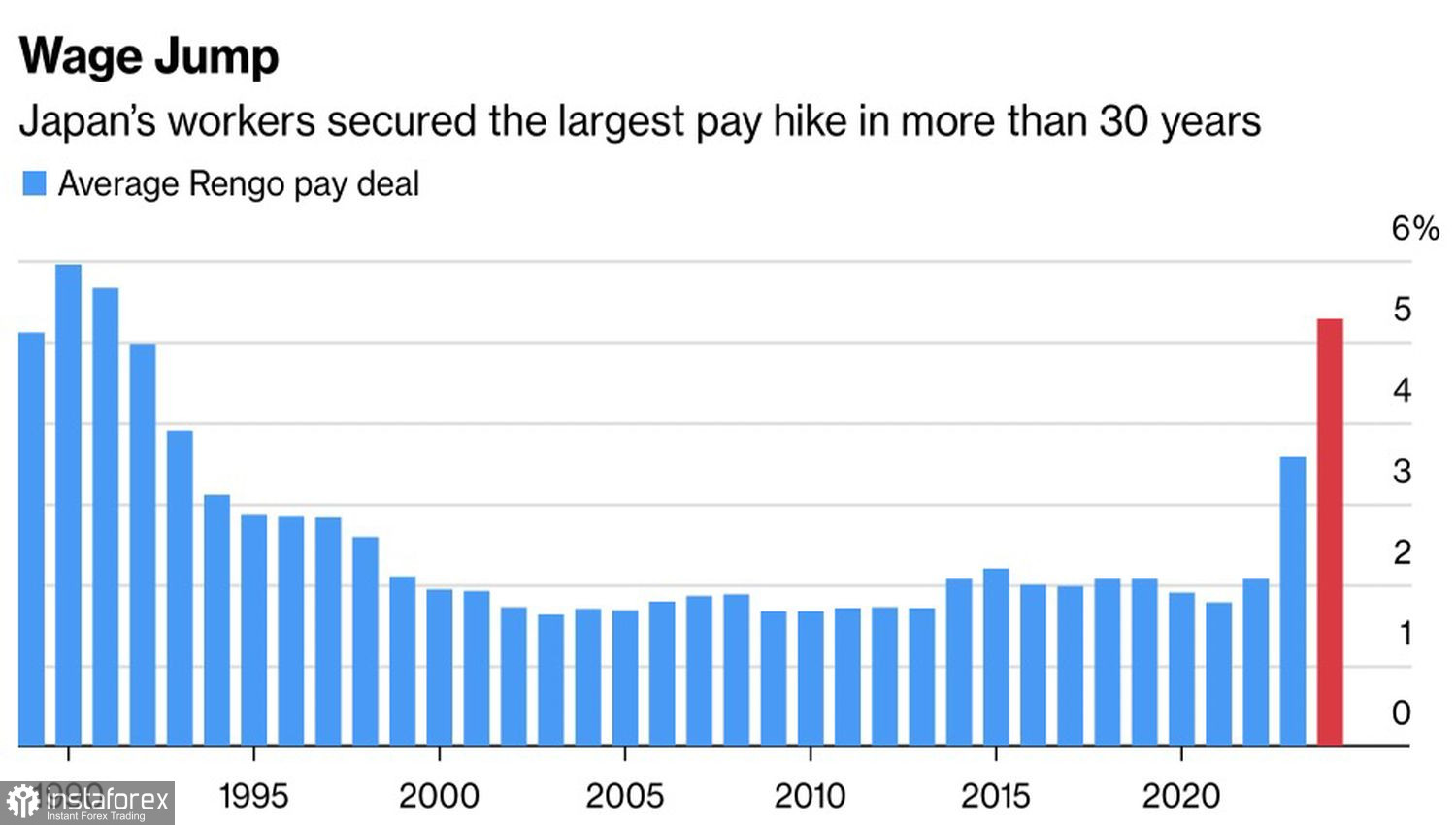

After it became known that unions had agreed with companies on the largest wage increase in the past 33 years, 90% of Bloomberg surveyed experts began to predict the Bank of Japan's withdrawal from negative rates as early as March. The rhetoric of BoJ Governor Kazuo Ueda and the fact that only seven members of the Board of Governors voted for the rate hike allowed the USD/JPY bulls to launch a swift attack.

Dynamics of Wages in Japan

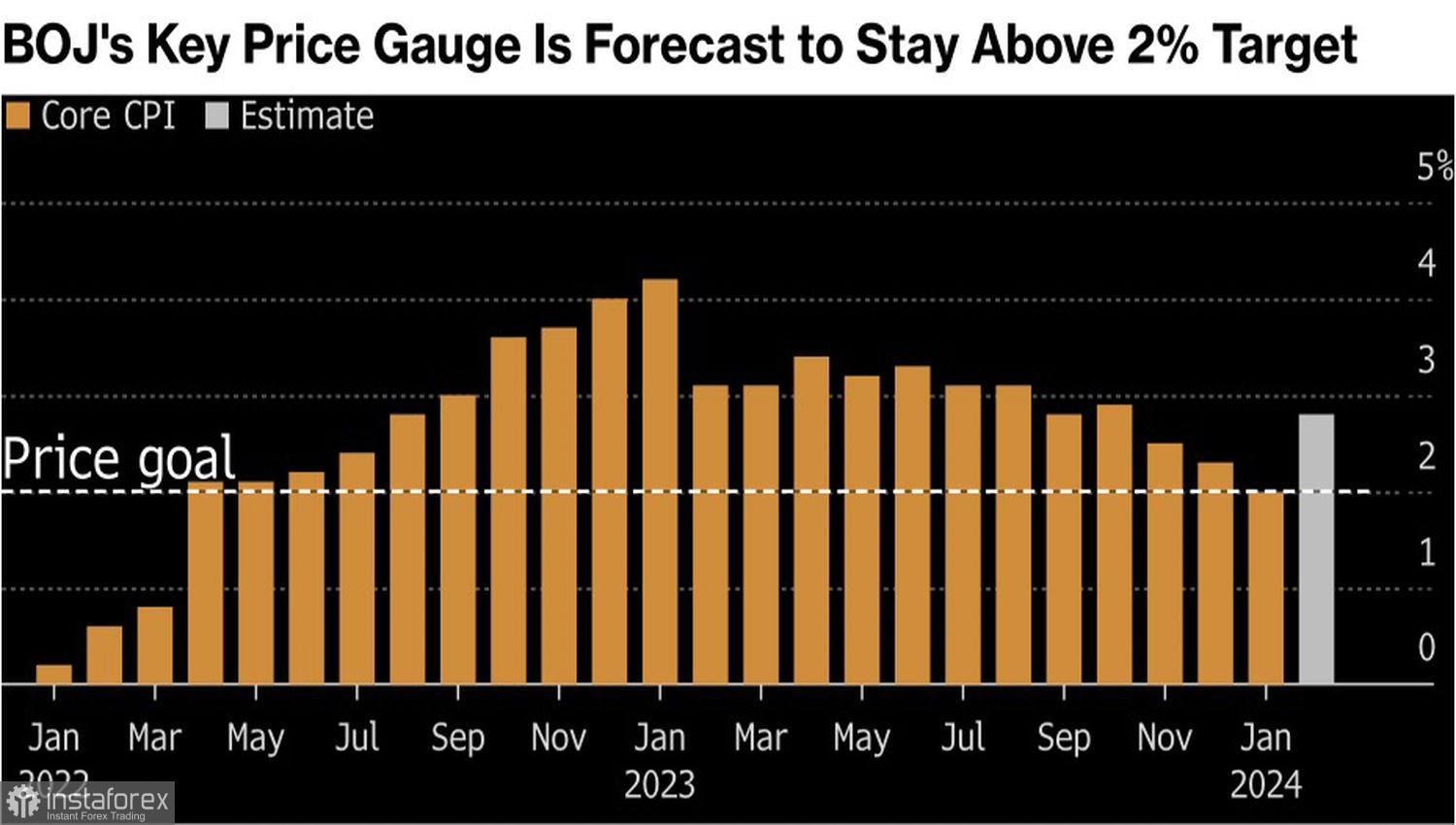

Ueda's statement that financial conditions remain accommodative convinced markets that the monetary tightening cycle would not be as swift as that of other central banks in 2021–2023. The Bank of Japan has shown that it is ready to measure seven times before cutting. It's easy to understand why: there are risks that inflation in Japan will slow down even further. In the face of policy dependence on data, the BoJ needs to exercise caution.

Similar thoughts arise when looking at the split in the votes of the Board of Governors: 7 against 2. Obviously, there are both "hawks" and "doves" there. The latter will surely oppose aggressive easing of monetary policy.

Inflation Dynamics in Japan

Tokyo's tortoise-paced move is accompanied by growing expectations that Washington will not rush with monetary expansion. The futures market sees a decrease in the federal funds rate to 4.7% in 2024. This is a smaller cut than indicated in the December FOMC forecast. Not surprisingly, against the backdrop of a resilient U.S. economy and two months of consecutive inflation pressure—in January and February.

The Federal Reserve is able to fuel the USD/JPY rally by raising the consensus estimate for the rate to 4.9% and higher. It implies not three acts of monetary expansion in 2024, but one less. If that's the case, U.S. stock indices will fall, Treasury yields will rise, and the dollar will strengthen against major world currencies. And the yen will be no exception.

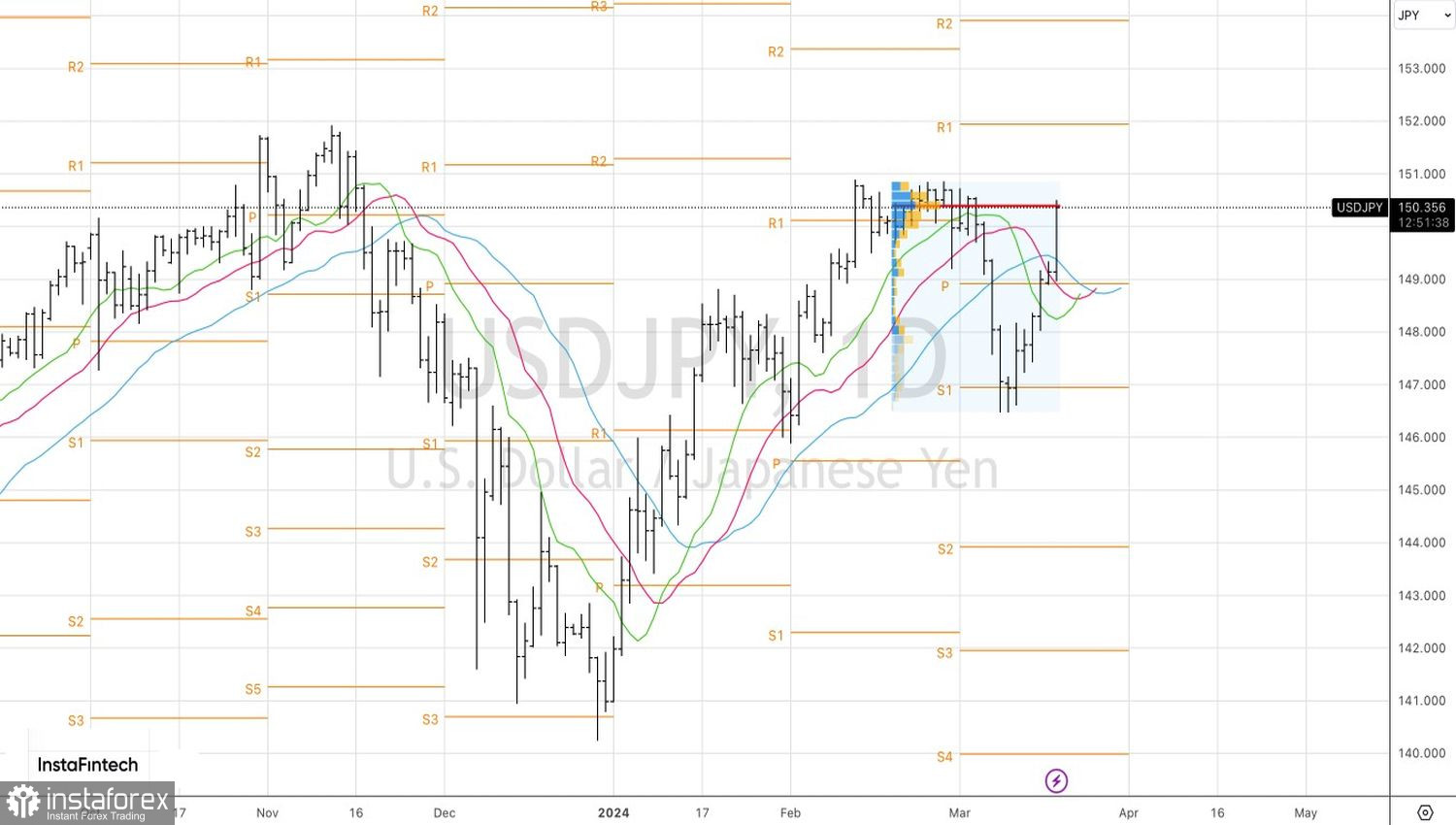

Technically, on the daily chart of USD/JPY, a rapid breakthrough by the bulls of dynamic resistance in the form of moving averages and a return of quotes to fair value in moments indicate the seriousness of buyers' intentions. The further fate of the pair will depend on their ability to maintain the positions gained. Closing above 150.35 will increase the risks of continuing the upward campaign to 151.9 and 153.3. Conversely, a drop below the important level will be a reason to sell.

*El análisis de mercado publicado aquí tiene la finalidad de incrementar su conocimiento, más no darle instrucciones para realizar una operación.

¡Los informes analíticos de InstaSpot lo mantendrá bien informado de las tendencias del mercado! Al ser un cliente de InstaSpot, se le proporciona una gran cantidad de servicios gratuitos para una operación eficiente.