Nella nostra squadra ci sono più di 7.000.000 trader! Ogni giorno ci impegniamo a far sì che il trading migliori. Conseguiamo grandi risultati e ci muoviamo in avanti.

Il riconoscimento da parte di milioni di trader in tutto il mondo rappresenta l'alta valutazione della nostra attività! Voi avete fatto la vostra scelta e noi faremo la nostra al fine di soddisfare le vostre aspettative!

Assieme siamo una grande squadra!

InstaSpot. Siamo orgogliosi di lavorare per voi!

Attore, campione del mondo di lotta libera e semplicemente un vero maciste russo! Persona venuta dal nulla. Persona che rispecchia i nostri obiettivi. Il segreto del successo di Taktarov consiste nel mirare continuamente al suo scopo.

Dischiudi anche tu tutti gli aspetti del tuo talento! Impara, prova, sbaglia, ma non fermarti!

InstaSpot - la storia delle tue vittorie inizia qui!

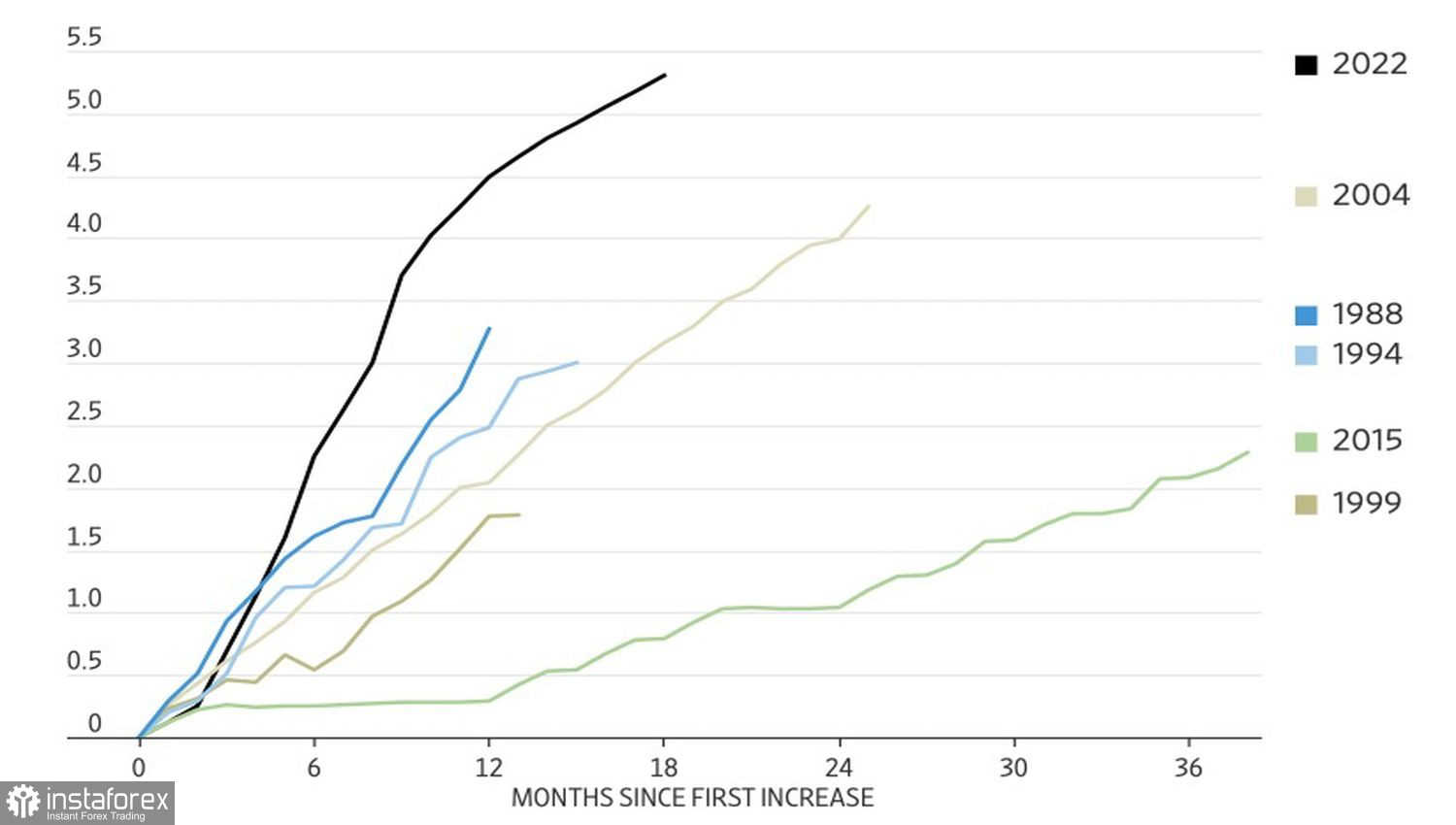

A year ago, most Bloomberg experts expected that the Federal Reserve would win the battle against inflation. To do so, they would have to sacrifice their own economy and push it into a recession. In reality, the U.S. GDP is growing rapidly, unemployment remains near half-century lows, and inflation is heading towards its target without hesitation. Could the Fed's policy have been so effective in achieving all of this?

Nobody's perfect, and the U.S. central bank has made mistakes over the past two years. In 2022, when forecasting inflation, it didn't take into account the post-pandemic rapid economic growth or the energy crisis caused by the war in Ukraine. For a long time, the Fed considered high prices to be a transient phenomenon, and only when it became clear that the CPI could exceed 8-9%, did it abandon that view. It then started tightening monetary policy in earnest.

The current cycle of monetary tightening has been the most aggressive in decades, but it wasn't until the end of 2024 that it became clear that high inflation was actually a temporary phenomenon. Its causes were related to supply shocks that the Fed couldn't influence. Supply chain disruptions due to COVID-19 and the war in Ukraine are gradually diminishing, and consumer prices are returning to the target level. In such conditions, keeping interest rates high is harmful to the economy, so the dovish pivot appears appropriate.

Now the Fed is forecasting a soft landing and three interest rate cuts of 75 basis points in total. This is the ideal scenario the central bank would like to see unfold. However, the risks are too high. In reality, the chances of a recession, a soft landing, and a new economic boom are approximately equal.

If inflation is caused by supply shocks and naturally returns to the 2% target on its own, then raising the federal funds rate by 525 bps in the current cycle will harm the economy. It will soon start to show serious signs of cooling and may even freeze. As the economy heads toward a downturn, demand for the U.S. dollar as a safe-haven currency will increase, causing EUR/USD to decline.

On the contrary, if most of the monetary tightening has already been absorbed by the economy due to Americans' excess savings, and wages are rising faster than inflation, GDP will accelerate. Ultimately, this will drive up inflation and force the Fed to return to raising the federal funds rate. In this scenario, EUR/USD will also fall.

There is only one scenario in which the main currency pair will rise, and that is a soft landing. But who can guarantee that it will happen?

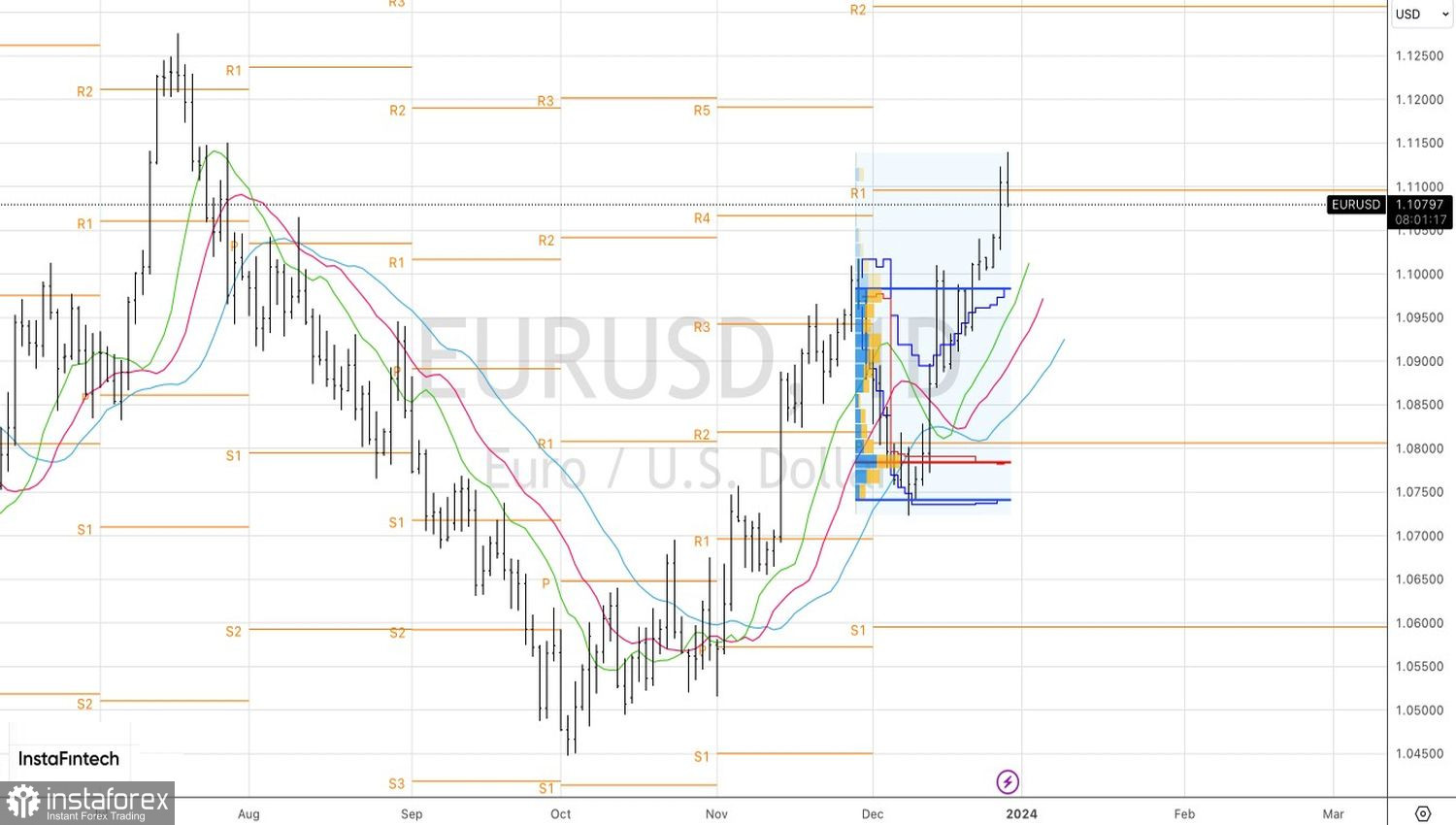

Technically, on the daily chart, EUR/USD is playing out a 20-80 pattern. After a wide-ranging bar was formed, an update of its high followed by a return below it signaled a bearish counterattack. As long as the pair is trading below 1.1095, there are reasons to sell it towards 1.104, 1.1015, and 1.0985.

*La presente analisi del mercato ha un carattere esclusivamente informativo e non rappresenta una guida per l`effettuazione di una transazione.

Le recensioni analitiche di InstaSpot ti renderanno pienamente consapevole delle tendenze del mercato! Essendo un cliente InstaSpot, ti viene fornito un gran numero di servizi gratuiti per il trading efficiente.