Đội ngũ của chúng tôi có hơn 7,000,000 thương nhân!

Hàng ngày chúng tôi làm việc cùng nhau để cải thiện việc giao dịch. Chúng tôi nhận được kết quả cao và luôn tiến lên phía trước.

Sự công nhận của hàng triệu thương nhân trên toàn thế giới là sự đánh giá tốt nhất cho công việc của chúng tôi! Bạn đã đưa ra quyết định của mình và chúng tôi sẽ làm mọi thứ cần thiết để đáp ứng mong đợi của bạn!

Chúng ta cùng với nhau sẽ là một nhóm tuyệt vời!

InstaSpot. Tự hào làm việc cho bạn!

Diễn viên, nhà vô địch mùa giải UFC 6 và là người hùng thật sự!

Người tự mình làm nên tất cả. Người đàn ông đáng kể học hỏi.

Bí mật đằng sau thành công của Taktarov là sự cố gắng liên tục hướng tới mục tiêu.

Hãy khai phá tất cả các mặt tài năng của bạn!

Khám phá, thử, thất bại - nhưng không bao giờ dừng lại!

InstaSpot. Câu chuyện thành công của bạn bắt đầu từ đây!

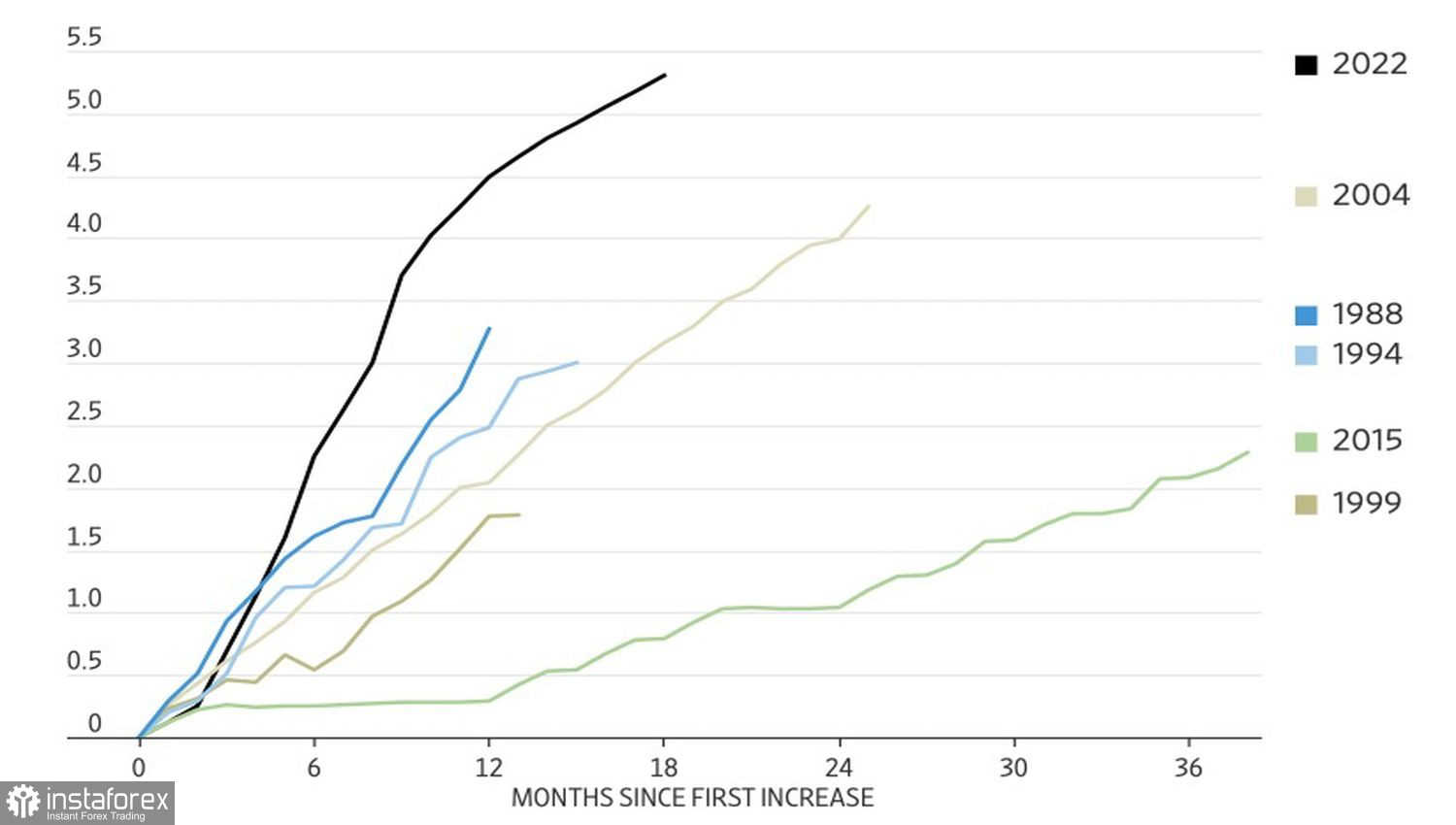

A year ago, most Bloomberg experts expected that the Federal Reserve would win the battle against inflation. To do so, they would have to sacrifice their own economy and push it into a recession. In reality, the U.S. GDP is growing rapidly, unemployment remains near half-century lows, and inflation is heading towards its target without hesitation. Could the Fed's policy have been so effective in achieving all of this?

Nobody's perfect, and the U.S. central bank has made mistakes over the past two years. In 2022, when forecasting inflation, it didn't take into account the post-pandemic rapid economic growth or the energy crisis caused by the war in Ukraine. For a long time, the Fed considered high prices to be a transient phenomenon, and only when it became clear that the CPI could exceed 8-9%, did it abandon that view. It then started tightening monetary policy in earnest.

The current cycle of monetary tightening has been the most aggressive in decades, but it wasn't until the end of 2024 that it became clear that high inflation was actually a temporary phenomenon. Its causes were related to supply shocks that the Fed couldn't influence. Supply chain disruptions due to COVID-19 and the war in Ukraine are gradually diminishing, and consumer prices are returning to the target level. In such conditions, keeping interest rates high is harmful to the economy, so the dovish pivot appears appropriate.

Now the Fed is forecasting a soft landing and three interest rate cuts of 75 basis points in total. This is the ideal scenario the central bank would like to see unfold. However, the risks are too high. In reality, the chances of a recession, a soft landing, and a new economic boom are approximately equal.

If inflation is caused by supply shocks and naturally returns to the 2% target on its own, then raising the federal funds rate by 525 bps in the current cycle will harm the economy. It will soon start to show serious signs of cooling and may even freeze. As the economy heads toward a downturn, demand for the U.S. dollar as a safe-haven currency will increase, causing EUR/USD to decline.

On the contrary, if most of the monetary tightening has already been absorbed by the economy due to Americans' excess savings, and wages are rising faster than inflation, GDP will accelerate. Ultimately, this will drive up inflation and force the Fed to return to raising the federal funds rate. In this scenario, EUR/USD will also fall.

There is only one scenario in which the main currency pair will rise, and that is a soft landing. But who can guarantee that it will happen?

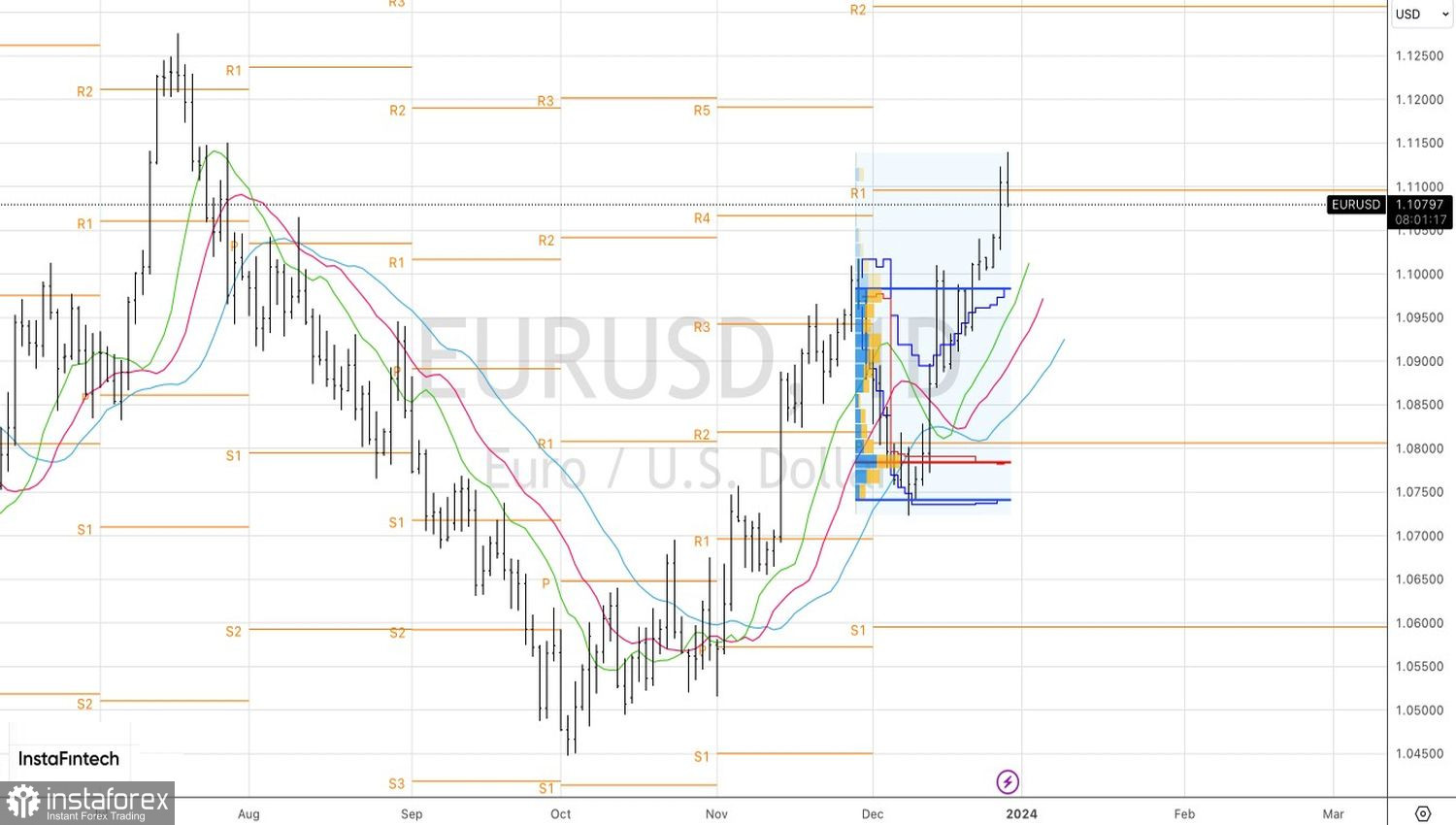

Technically, on the daily chart, EUR/USD is playing out a 20-80 pattern. After a wide-ranging bar was formed, an update of its high followed by a return below it signaled a bearish counterattack. As long as the pair is trading below 1.1095, there are reasons to sell it towards 1.104, 1.1015, and 1.0985.

*Phân tích thị trường được đăng tải ở đây có nghĩa là để gia tăng nhận thức của bạn, nhưng không đưa ra các chỉ dẫn để thực hiện một giao dịch.

InstaSpot analytical reviews will make you fully aware of market trends! Being an InstaSpot client, you are provided with a large number of free services for efficient trading.