Our team has over 7,000,000 traders!

Every day we work together to improve trading. We get high results and move forward.

Recognition by millions of traders all over the world is the best appreciation of our work! You made your choice and we will do everything it takes to meet your expectations!

We are a great team together!

InstaSpot. Proud to work for you!

Actor, UFC 6 tournament champion and a true hero!

The man who made himself. The man that goes our way.

The secret behind Taktarov's success is constant movement towards the goal.

Reveal all the sides of your talent!

Discover, try, fail - but never stop!

InstaSpot. Your success story starts here!

New Zealand's GDP for Q4 rose by just 0.2% quarter-on-quarter, below both market expectations and those of the Reserve Bank of New Zealand (RBNZ). ANZ Bank forecasts GDP growth of 0.7% year-on-year in 2026, but further deterioration is possible if rising energy prices are compounded by problems with fertilizer supply and increasing fertilizer costs—which now appears highly likely. For New Zealand's agricultural sector, this would be a very significant blow, affecting not only production levels but also exports.

The RBNZ will hold its next meeting on April 8, and it is already clear that positive outcomes are unlikely. Whatever the bank does with its interest rate, it cannot stop rising oil prices or short-term inflation. Nor can it prevent the associated impact on economic growth. Changes in monetary policy will have only a limited effect on these short-term developments.

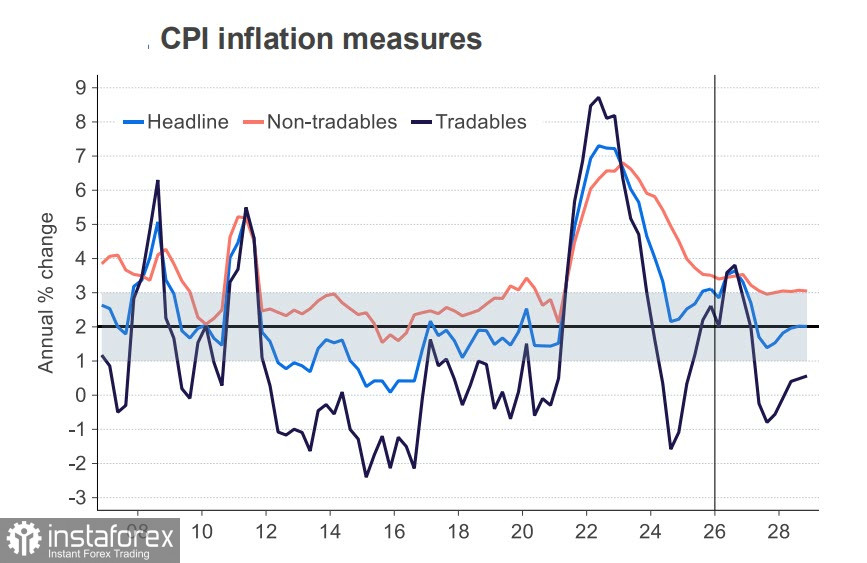

As fuel prices continue to rise, inflation forecasts are also increasing. BNZ expects CPI to reach 3.0% in the first quarter and 4.2% in the second quarter of 2026. Beyond that, everything will depend on the extent of the damage in the Gulf and disruptions in energy logistics, which are currently impossible to predict.

There is very little data expected this week: on Friday, only the ANZ-RM consumer confidence index is due for release. Until recently, there had been an upward trend, but it is likely to decline in March, while consumer inflation expectations, on the contrary, are expected to rise. High fuel prices reduce household purchasing power and business profitability, meaning GDP forecasts are likely to be revised downward in the near future. Fitch Ratings, while maintaining New Zealand's credit rating at AA+, has downgraded the outlook from stable to negative. This is the first warning sign, and others will likely follow.

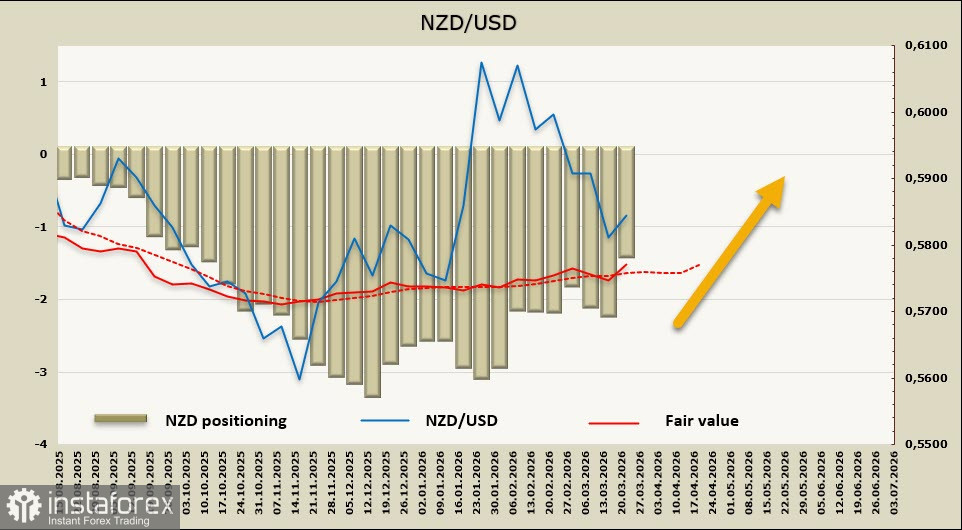

The net short position on the NZD decreased by 0.9 billion over the reporting week to -1.35 billion, but positioning remains bearish. The estimated price, amid a temporary easing of tensions following statements by Trump, is attempting to move upward.

For NZD/USD, two main scenarios are possible, and it is not possible to predict which one will materialize. In the case of further escalation in the Gulf, the kiwi will inevitably decline toward 1.5533, as the level of economic risk will increase, and even rate hikes will not stop the decline. If the conflict ends and the consequences are reassessed, growth may resume—provided the impact on GDP is not severe enough to prevent the RBNZ from raising rates. In this case, the nearest target will be 0.5887, followed by further growth toward 0.6086.

*এখানে পোস্ট করা মার্কেট বিশ্লেষণ আপনার সচেতনতা বৃদ্ধির জন্য প্রদান করা হয়, ট্রেড করার নির্দেশনা প্রদানের জন্য প্রদান করা হয় না।

ইন্সটাফরেক্স বিশ্লেষণমূলক পর্যালোচনাগুলো আপনাকে মার্কেট প্রবণতা সম্পর্কে পুরোপুরি সচেতন করবে! ইন্সটাফরেক্সের একজন গ্রাহক হওয়ায়, দক্ষ ট্রেডিং এর জন্য আপনাকে অনেক সেবা বিনামূল্যে প্রদান করা হয়।