¡La leyenda en el equipo de InstaSpot!

¡Leyenda! ¿Cree que es una retórica grandilocuente? Pero, ¿cómo deberíamos llamar a un hombre, que se convirtió en el primer asiático en ganar el campeonato mundial de ajedrez júnior a los 18 años y en el primer Gran Maestro indio a los 19 años? Ese fue el comienzo de un camino difícil hacia el título de Campeón del Mundo para Viswanathan Anand, el hombre que se convirtió en parte de la historia del ajedrez para siempre. ¡Ahora una leyenda más en el equipo de InstaSpot!

Borussia es uno de los clubes de fútbol con más títulos en Alemania, que ha demostrado repetidamente a los fanáticos: el espíritu de competencia y liderazgo que ciertamente conducirán al éxito. Opere de la misma manera que los profesionales del deporte: con confianza y de forma activa. ¡Mantenga un "pase" del Borussia FC y lidere con InstaSpot!

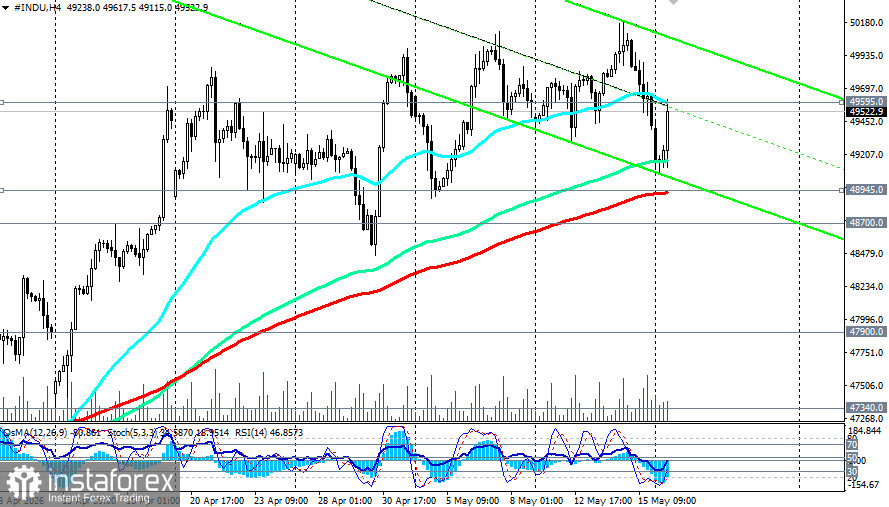

In early trade on Monday, DJIA futures tested an important short-term resistance level at 49,595, recovering from a local nine-day low of 49,070 reached in the morning. Prices have preserved bullish momentum, consolidating in a range after a failed attempt earlier this month to hold above the psychologically important 50,000 level.

Investors are frozen in anxious anticipation as two powerful countervailing forces play out: on one side, a hawkish shock from US inflation data and rising bond yields; on the other, hopes for diplomatic progress in the Middle East that have so far limited further declines.

Fundamental backdrop: ideal storm for equities

The primary driver of pressure on equity markets remains the fallout from last week's shocking US inflation prints.

Key indicators

- Annual CPI inflation accelerated to 3.8%, the highest level since May 2023.

- Producer prices (PPI) jumped to 6.0% year on year, the strongest rise since 2022 and well above forecasts.

- The 10-year US Treasury yield responded immediately, spiking to a one-year high of about 4.6% and continuing to weigh on long-duration assets.

This inflation shock has materially altered the monetary policy landscape. Markets have fully discounted rate cuts in 2026 and now price roughly a 50% probability of a Federal Reserve rate increase by year-end.

The Senate confirmed Kevin Warsh as the new Fed chair. Warsh, associated with a hawkish stance, balance-sheet reductions, and stricter inflation control, formally succeeded Jerome Powell after the end of Powell's term. His appointment cements expectations that restrictive policy will persist longer than previously assumed. Susan Collins, president of the Boston Fed, has already indicated she can envision a scenario that requires some policy tightening to return inflation to target.

At the same time, markets remain attentive to developments in the Middle East. Tensions persist: a drone strike ignited a fire at the Barakah nuclear plant in the United Arab Emirates, and Saudi Arabia intercepted drones launched from Iraq. Conversely, there are signs diplomacy is not completely closed. Reports indicate technical teams from Iran and Oman met to discuss a mechanism for safe transit through the Strait of Hormuz, and Iran's foreign ministry confirmed that indirect diplomatic channels with the United States remain functional. Those reports triggered a temporary pullback in oil prices and offered some support to futures.

Technical snapshot

From a technical perspective, DJIA futures are at a critical threshold while still retaining a bullish bias after the retreat from highs above 50,100.

On the four-hour chart, the price is consolidating below a key moving average at 49,595 (the 50-period exponential moving average, which also corresponds to the 200-period EMA on the one-hour chart) and is facing pressure from above.

The RSI (14) sits in the 45–46 zone, indicating prevailing bearish momentum, while the OsMA and stochastic indicators are attempting to exit oversold territory.

The short-term outlook remains bearish while the price trades below resistance at 49,595. A breakout and sustained close above the local resistance at 49,800 would keep alive the prospect of a retest of the 50,000 psychological level and further gains.

Key events ahead

Market focus will shift next week from macroeconomic releases to key corporate earnings.

- Wednesday, May 20: FOMC minutes publication — a key trigger that will clarify the extent of hawkish sentiment within the Fed.

- Wednesday, May 20: Nvidia earnings — the report will be the principal test for the technology sector and the AI rally.

- Thursday, May 21: Walmart and Target earnings — the retail reports will serve as a key gauge of consumer resilience amid high fuel prices and inflation.

- Ongoing: US-Iran and Oman-Iran talks — any development could rapidly move oil prices and trigger market volatility.

Conclusion

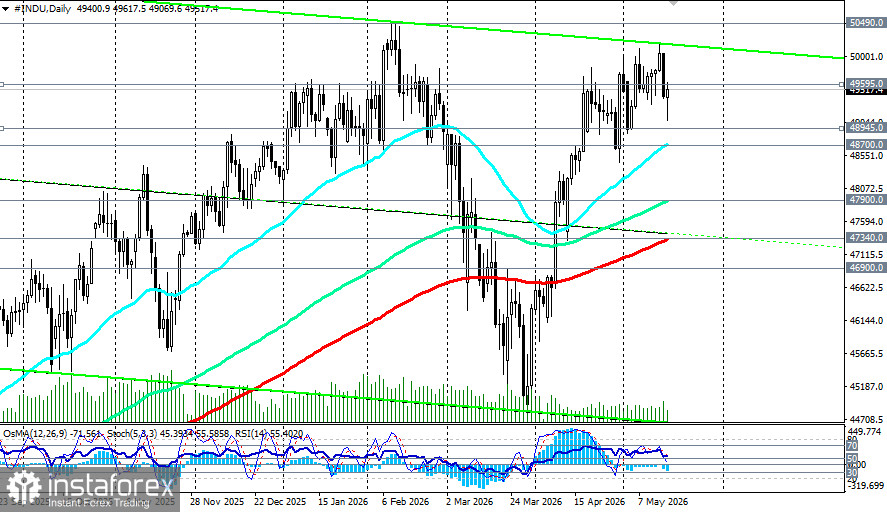

The Dow Jones is under substantial pressure. The inflation shock (with PPI at 6.0%) and a hawkish pivot at the Fed create a classic bearish backdrop, pushing bond yields toward new highs. The 10-year Treasury yield has settled near 4.6%, a level that typically weighs on equities, especially long-duration technology names.

The 49,000–49,600 zone will be the battleground in the coming days. A breakdown below that area would likely trigger another wave of selling toward 48,700 (the daily EMA50) and beyond.

Investors should monitor the FOMC minutes on Wednesday and the earnings reports from Nvidia and major retailers. Any confirmation of a hawkish tilt or disappointment in corporate results could intensify the correction. A "sell on rallies" strategy toward resistance near 49,600 remains the preferred stance, while buying is justified only after a firm close above 50,000.

*El análisis de mercado publicado aquí tiene la finalidad de incrementar su conocimiento, más no darle instrucciones para realizar una operación.

¡Los informes analíticos de InstaSpot lo mantendrá bien informado de las tendencias del mercado! Al ser un cliente de InstaSpot, se le proporciona una gran cantidad de servicios gratuitos para una operación eficiente.