¡Nuestro equipo cuenta con más de 7,000,000 operadores!

Cada día, trabajamos juntos para mejorar las operaciones. Obtenemos grandes resultados y seguimos adelante.

El reconocimiento de millones de operadores en todo el mundo es el mejor agradecimiento a nuestro trabajo! ¡Usted hizo su elección y haremos todo lo que esté a nuestro alcance para satisfacer sus expectativas!

¡Juntos somos un gran equipo!

InstaSpot. ¡Orgulloso de trabajar para usted!

¡Actor, 6 veces ganador del torneo UFC y un verdadero héroe!

El hombre que se hizo a sí mismo. El hombre que sigue nuestro camino.

El secreto detrás del éxito de Taktarov es el constante movimiento hacia el objetivo.

¡Revele todo los lados de su talento!

Descubra, intente, fracase, ¡pero nunca se rinda!

InstaSpot. ¡Su historia de éxito comienza aquí!

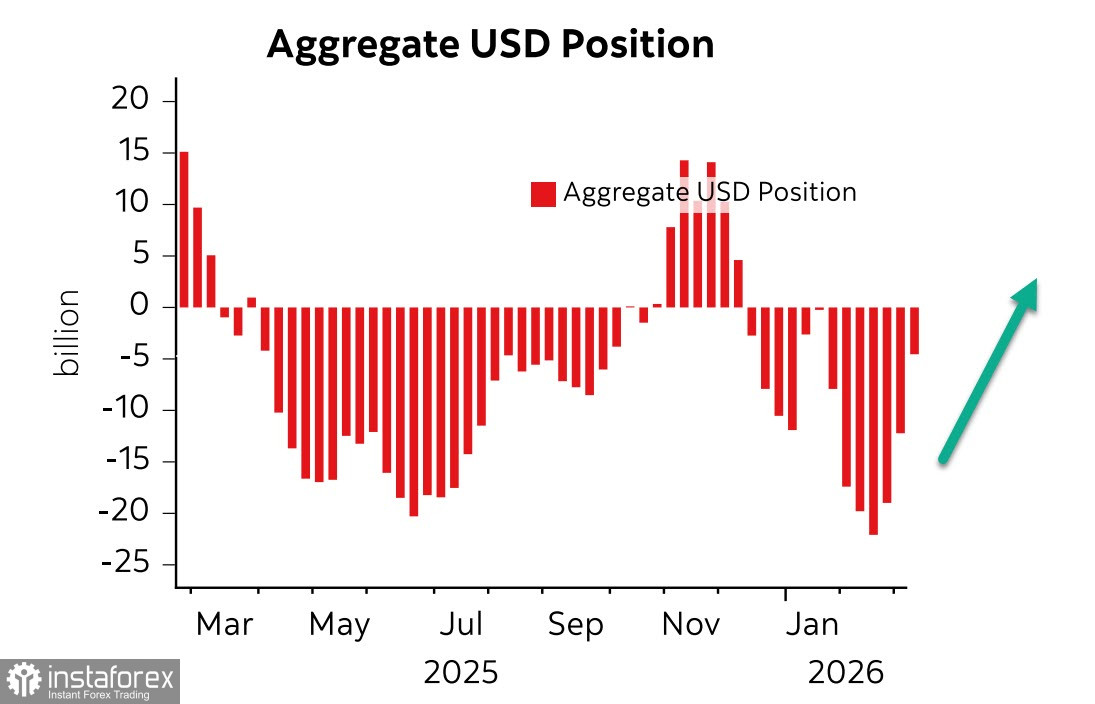

Speculative positioning is rapidly shifting in favor of the US dollar. According to the latest CFTC report, aggregate short dollar positions decreased by $7.5 billion over the week, with almost all the repositioning coming out of the euro and the yen — the two currencies most vulnerable to rising oil and gas prices, since the main energy supply routes to the EU and Japan are tied to the Persian Gulf.

If Japan has little choice, Europe is a textbook case of political folly and energy self-sabotage. Europe voluntarily gave up reliable supplies of cheap energy and simultaneously undermined its own nuclear generation, creating obvious vulnerability.

If the war in the Gulf drags on, the euro's prospects are very poor — and speculators are pricing that in by rapidly trimming long euro exposure.

For now, the market prefers to hope that the conflict will be short and that oil and LNG flows from the Gulf will resume. This is evident in the moderate oil price jump, despite the sharp supply curbs.

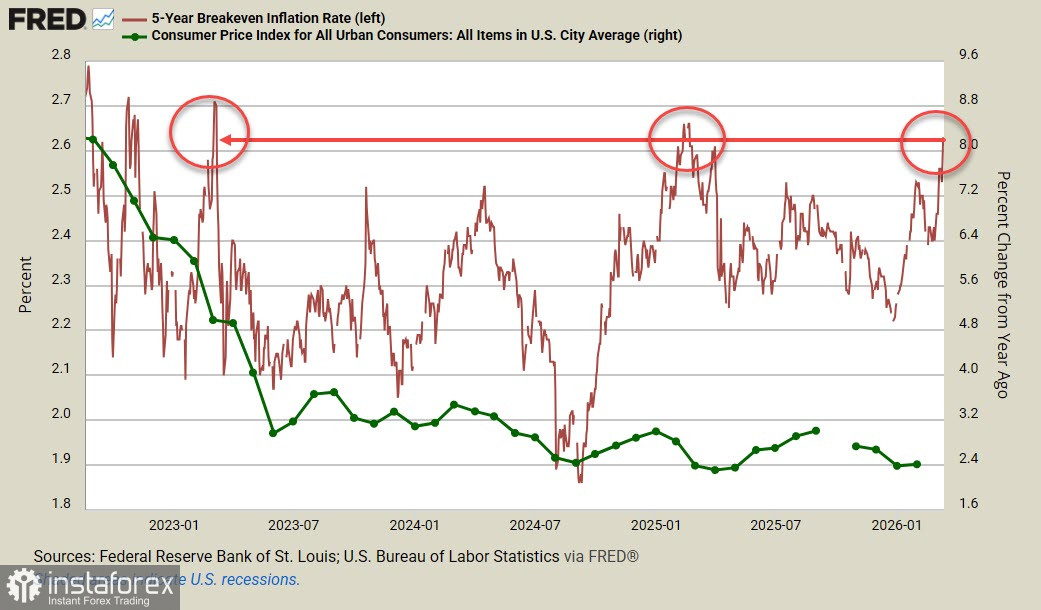

As for the US economic picture, pessimism is already winning out. Q4 GDP was revised down from 1.4% to 0.7%, worsening an already negative picture suggested by very weak labor market reports in recent months. Inflation dynamics remain mixed: core PCE rose by 0.4% in January and by 3.1% year-on-year, 0.1pp higher than in December. Durable goods orders were flat in January, a clear sign of weak consumer demand, while the 5-year TIPS yield is near a three-year high, which means that business sees the risk of further inflation acceleration.

Cooling consumer demand will widen the budget deficit, government debt, and the current account shortfall. In the long run, that poses major problems for the US dollar, and we believe that ultimately it should weaken. The current strength is only a short-term market reaction. A growing current account deficit increases the US economy's dependence on foreign capital, and if equity markets, for example, start to slide from record highs, capital inflows would abate, with the deficit widening further.

A likely slowdown in GDP growth would almost certainly produce such a scenario, and, combined with expected higher inflation, will put both the US government and the Federal Reserve in an even more difficult position. Already, Fed funds futures imply just one rate cut this year — and that only in December — so markets are pricing in a very high inflation threat. That, in turn, points to the prospect of stagflation — the worst-case outcome for any central bank or government.

We assume that the US dollar will remain strong in the short term, until there is credible hope the Gulf war will end. Over the longer term, however, an increasing number of indicators point to its eventual weakening.

*El análisis de mercado publicado aquí tiene la finalidad de incrementar su conocimiento, más no darle instrucciones para realizar una operación.

¡Los informes analíticos de InstaSpot lo mantendrá bien informado de las tendencias del mercado! Al ser un cliente de InstaSpot, se le proporciona una gran cantidad de servicios gratuitos para una operación eficiente.