¡La leyenda en el equipo de InstaSpot!

¡Leyenda! ¿Cree que es una retórica grandilocuente? Pero, ¿cómo deberíamos llamar a un hombre, que se convirtió en el primer asiático en ganar el campeonato mundial de ajedrez júnior a los 18 años y en el primer Gran Maestro indio a los 19 años? Ese fue el comienzo de un camino difícil hacia el título de Campeón del Mundo para Viswanathan Anand, el hombre que se convirtió en parte de la historia del ajedrez para siempre. ¡Ahora una leyenda más en el equipo de InstaSpot!

Borussia es uno de los clubes de fútbol con más títulos en Alemania, que ha demostrado repetidamente a los fanáticos: el espíritu de competencia y liderazgo que ciertamente conducirán al éxito. Opere de la misma manera que los profesionales del deporte: con confianza y de forma activa. ¡Mantenga un "pase" del Borussia FC y lidere con InstaSpot!

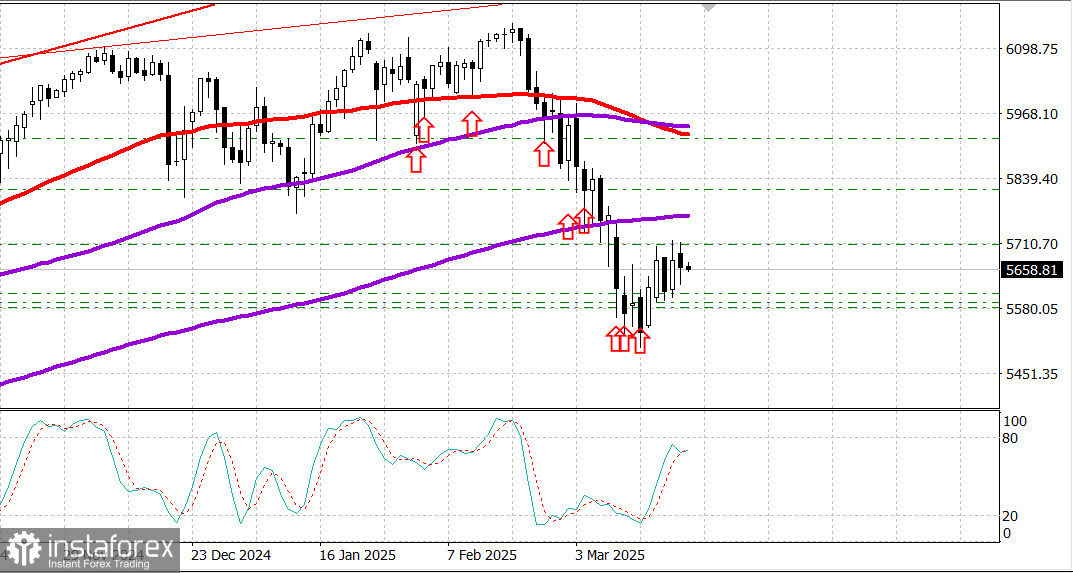

S&P 500

Overview for March 21

The US market entered a phase of consolidation on Thursday as it struggled to define its next direction.

Major US indices on Thursday: Dow: -0.1%, NASDAQ: -0.3%, S&P 500: -0.2%, S&P 500: 5,662, trading range: 5,500-6,000.

The rally that followed the Fed's decision and statement lost momentum on Thursday.

There was an attempt to extend the upward move, but it eventually faded, particularly as mega-cap stocks pulled back. Investors appeared preoccupied with uncertainty surrounding the economic outlook, lacking clear answers.

Still, there was positive economic data during the session. Existing home sales surprised to the upside in February as buyers responded to increased supply.

This was a constructive signal, supported by the lack of any major change in weekly initial jobless claims, which remain at levels consistent with a strong labor market.

These reports reinforced Fed Chair Powell's comments yesterday that "strong data," unlike weak survey-based indicators, remains a fairly reliable gauge of economic activity.

Nevertheless, the looming threat of mutual tariffs set to take effect on April 2, coupled with the Fed's somewhat confusing outlook—lower GDP growth and higher inflation projected for 2025—seemed to dampen enthusiasm for building on Wednesday's gains.

Overall, Thursday was marked by a lack of conviction on either side of the market.

Four S&P 500 sectors ended the day in positive territory, none rising more than 0.4%. Seven sectors closed lower, with the largest decline limited to 0.6%.

Energy and utilities led the gains, while materials posted the biggest drop.

The information technology sector, the most heavily weighted in the market, ended down 0.5%. It was a relative laggard throughout the session, largely due to weakness in Accenture (ACN 300.76-23.71, -7.3%) following its earnings report, Apple (AAPL 214.10, -1.14, -0.5%) as reports suggested the company retreated in the AI leadership rankings, and semiconductor stocks.

The Philadelphia Semiconductor Index fell by 0.7%, which could have been worse if not for the strong performance of NVIDIA (NVDA), which rose by 0.9%.

The Treasury market showed signs of volatility as well. Earlier, the 10-year yield fell to 4.17% from Wednesday's close of 4.26%, then rebounded to 4.25%, before settling at 4.2%.

Like other capital markets, US Treasuries reacted to a wave of central bank decisions following the FOMC announcement, including:

Economic data overview:

Initial jobless claims for the week ending March 15 rose by 2,000 to 223,000 (consensus: 220,000).

Continuing claims for the week ending March 8 rose by 33,000 to 1.892 million.

Key takeaway: This period covers the survey week for the upcoming employment report, and low levels of jobless claims may prompt economists to forecast another solid gain in nonfarm payrolls.

The current account deficit narrowed to $303.9 billion in the fourth quarter (consensus: -$334.0B) from a revised -$310.3 billion (up from -$310.9B).

The Philadelphia Fed Index fell to 12.5 in March (consensus: 10.0) from 18.1 in February. The expansion/contraction threshold is 0.0, meaning business activity in the Philadelphia Fed region grew in March, albeit at a slower pace than the previous month.

Existing home sales rose 4.2% month-on-month in February to a seasonally adjusted annual rate of 4.26 million (consensus: 3.95M), up from a revised 4.09M in January. On an annual basis, sales declined by 1.2%, but the key point is that sales increased, while consensus had expected a 3.2% monthly drop.

The surprising strength in the housing market suggests a release of pent-up demand, with more inventory available and buyers adjusting to higher mortgage rates.

Leading indicators declined by 0.3% in February (consensus: -0.2%), following a revised -0.2% in January (originally -0.3%).

No major US economic data is scheduled for Friday.

Energy: Brent crude rose to $72.20, up nearly $1 on Friday. It rally was driven by the news that US President Trump called on the Senate to authorize military strikes on Iran. Earlier, Trump had issued an ultimatum to Iran: sign a deal with the US to halt its nuclear weapons program, or face strikes on nuclear and military sites within two months.

Conclusion: The US market still has the potential for further gains. It is recommended to hold long positions from support levels and expect the S&P 500 to head towards the 6,000 level.

*El análisis de mercado publicado aquí tiene la finalidad de incrementar su conocimiento, más no darle instrucciones para realizar una operación.

¡Los informes analíticos de InstaSpot lo mantendrá bien informado de las tendencias del mercado! Al ser un cliente de InstaSpot, se le proporciona una gran cantidad de servicios gratuitos para una operación eficiente.