Kumpulan kami mempunyai lebih daripada 7,000,000 pedagang!

Setiap hari kami bekerjasama untuk meningkatkan perdagangan. Kami mendapat keputusan yang tinggi dan bergerak ke hadapan.

Pengiktirafan oleh berjuta-juta pedagang di seluruh dunia adalah penghargaan terbaik untuk kerja kami! Anda membuat pilihan anda dan kami akan melakukan segalanya yang diperlukan untuk memenuhi jangkaan anda!

Kami adalah kumpulan yang terbaik bersama!

InstaSpot. Berbangga bekerja untuk anda!

Pelakon, juara kejohanan UFC 6 dan seorang wira sebenar!

Lelaki yang membuat dirinya sendiri. Lelaki yang mengikut cara kami.

Rahsia di sebalik kejayaan Taktarov adalah pergerakan berterusan ke arah matlamat.

Dedahkan semua segi bakat anda!

Cari, cuba, gagal - tetapi tidak pernah berhenti!

InstaSpot. Kisah kejayaan anda bermula di sini!

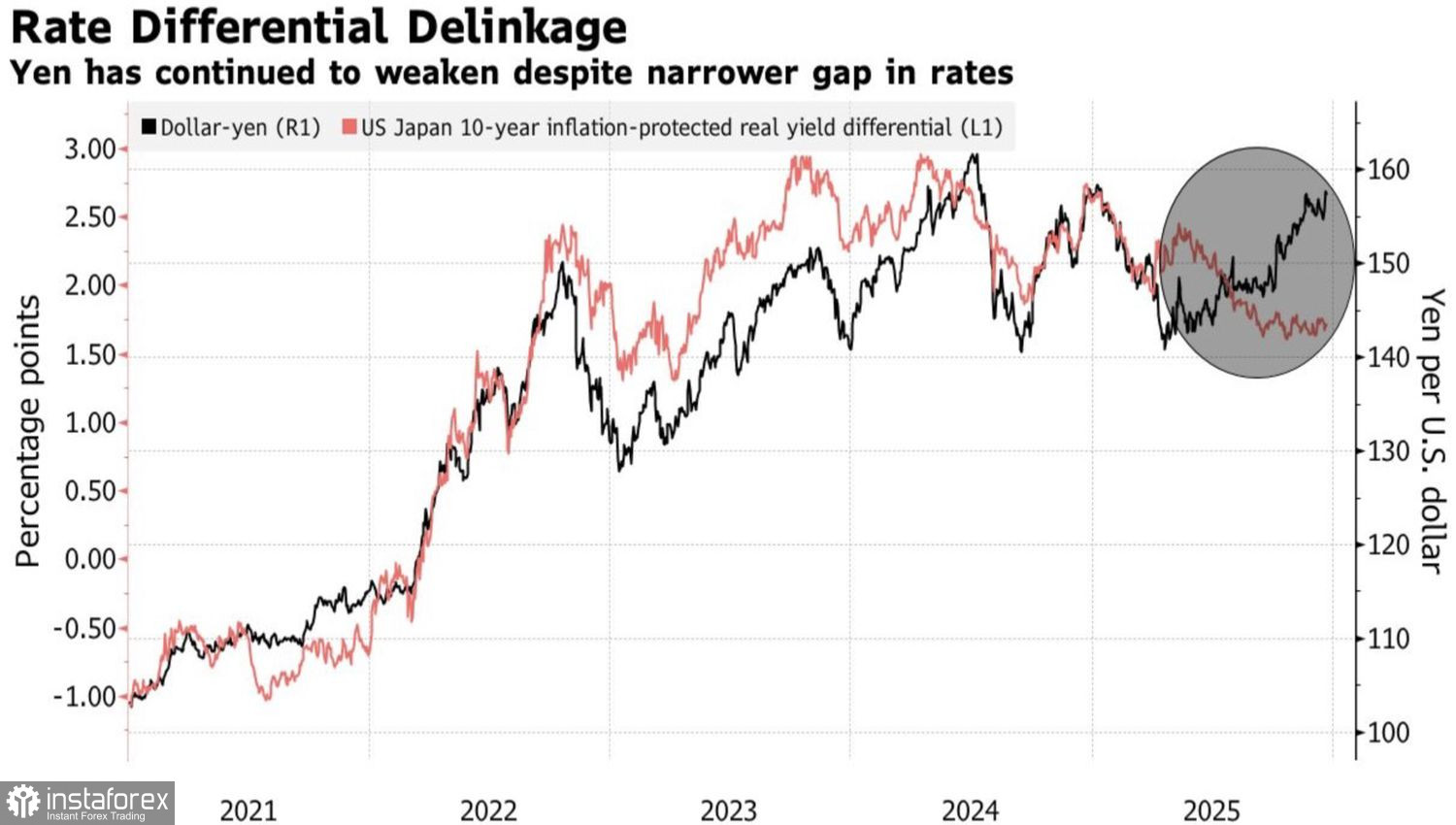

Don't tempt fate! The strongest government intervention since Sanae Takaichi took office as Prime Minister has seriously frightened the USD/JPY "bulls." Finance Minister Satsuki Katayama chose the right moment to talk about Tokyo's free hands to counter speculators. If Japan were to intervene in the forex market during the thin Christmas market, a sharp strengthening of the yen would be guaranteed. So, isn't it better to stay away from selling the Japanese currency?

Fears about a weak yen outweigh concerns about the increasing cost of servicing colossal debts. As an energy-importing nation, Japan cannot afford USD/JPY at 160 and above. At such an exchange rate, inflation risks accelerating further, and combating inflation is Takaichi's main priority. At the same time, Donald Trump also wants a weaker U.S. dollar. It is not surprising that the government ignored the overnight rate increase to 0.75%, the highest level since 1995.

Given the inadequate surge in USD/JPY in response to tightening monetary policy, the Cabinet has a strong case for intervention. Officials state that the yen's movements on the Forex market do not reflect fundamental realities. Indeed, the divergence in monetary policy between the Federal Reserve and the Bank of Japan should narrow bond yield spreads and contribute to a decline in the pair's quotes. However, the charts show a significant divergence, indicating the yen's clear undervaluation.

However, there is a view in the market that little depends on the BoJ. The weakening of the yen is a result of investors' doubts about Japan's ability to maintain order in its fiscal house. The rise in local bond yields confirms this. Traders demand a higher risk premium for holding assets from Japan. At the same time, capital outflows contribute to the rise in USD/JPY quotes.

U.S. assets indeed appear more attractive. High inflation in Japan makes real yields on local bonds negative. Moreover, if both the Fed and the BoJ maintain borrowing costs at previous levels, this creates ideal conditions for carry trades and for selling the yen as a funding currency.

As a result, after the Christmas holidays, the government will have to fight the markets. And I fear that without the help of the White House and the Fed, it is doomed to failure. In previous successful interventions, Tokyo showed signs of a weakening U.S. dollar.

Technically, on the daily chart, USD/JPY is forming Double Top and Expanding Wedge patterns. Without a decline in quotes below the line 1-3 near the mark of 154.5, it is premature to talk about a significant pullback. A return above the fair value at 156.3 will be a basis for buying.

* Analisis pasaran yang disiarkan di sini adalah bertujuan untuk meningkatkan kesedaran anda, tetapi tidak untuk memberi arahan untuk membuat perdagangan.

Kajian analisis InstaSpot akan membuat anda mengetahui sepenuhnya aliran pasaran! Sebagai pelanggan InstaSpot, anda disediakan sejumlah besar perkhidmatan percuma untuk dagangan yang cekap.