La leggenda nel team InstaSpot!!

Legenda! Pensi che sia troppo patetico? Ma come dobbiamo chiamare un uomo, che è diventato il primo dell'Asia a vincere il campionato mondiale di scacchi a 18 anni e che è diventato il primo Gran Maestro indiano a 19? Fu l'inizio di un duro cammino verso il titolo di campione del mondo, l'uomo che divenne per sempre una parte della storia di scacchi. Un'altra leggenda nel team InstaSpot!

Il Borussia è una delle squadre di calcio più titolate in Germania, che ha ripetutamente dimostrato ai tifosi che lo spirito di competizione e leadership porta al successo. Fai trading nello stesso modo in cui lo fanno i professionisti dello sport - fiduciosamente e attivamente. Segui il Borussia FC e sii avanti con InstaSpot!

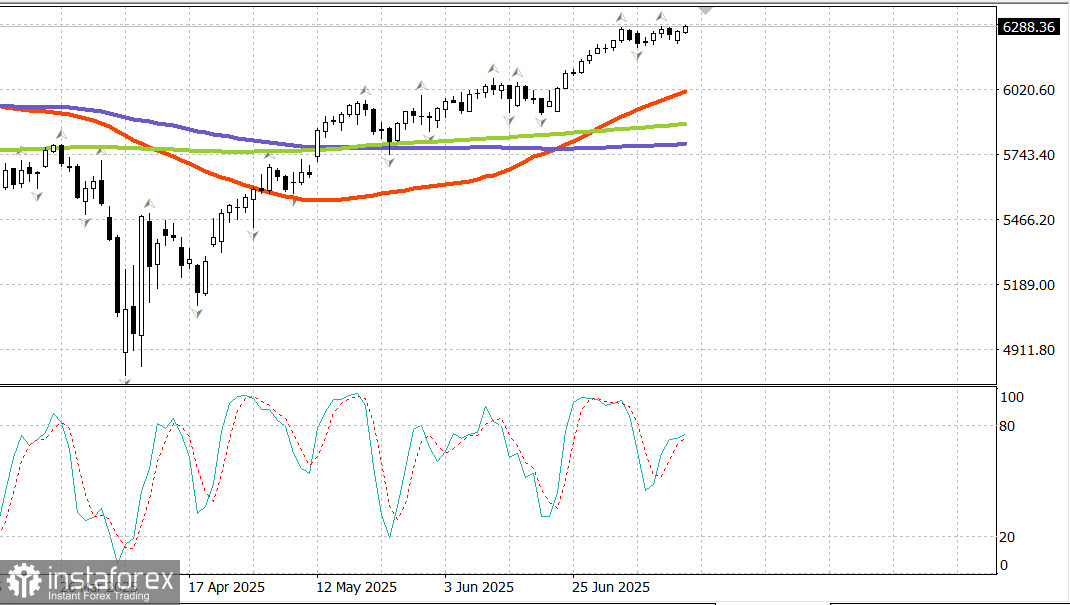

S&P500

Major stock indices standing tall near all-time highs

Snapshot of the key US stock indices on Monday:

The US stock market bounced off early-session lows following new tariff headlines. Steady trading helped the major indices finish the day with modest gains, and the Nasdaq closed at a new all-time high.

The proposed 30% tariff on the EU and Mexico starting August 1 was enough to trigger a sluggish market opening. However, as expected, the market showed resilience to tariff-related news, which has yet to disrupt its uptrend.

The policymakers of the EU Commission and the President of Mexico expressed willingness to negotiate a more favorable trade deal before the August 1 deadline. This sentiment helped contain selling pressure during the session.

Additionally, markets remained unfazed by President Trump's announcement of new tariffs on Russia—up to 100% starting September 1—should Russia fail to agree to a ceasefire.

Despite the relatively positive tone around tariffs, Monday's gains were modest. Investor confidence was cautious ahead of key economic reports and a wave of corporate earnings this week.

High-impact reports due this week:

Several major banks, including Wells Fargo (WFC 83.43, +0.88, +1.1%), Citigroup (C 87.50, +0.77, +0.9%), and JPMorgan Chase (JPM 288.70, +1.84, +0.6%), will release earnings before Tuesday's market open.

Thanks to positioning ahead of earnings, the financial sector (+0.7%) was among the day's leaders. The communication services sector (+0.7%) also led on Monday:

Netflix (NFLX 1260.81, +15.70, +1.26%) traded higher ahead of Thursday's earnings report.

The sector also benefited from gains in Alphabet (GOOG 182.76, +1.45, +0.8%) and Meta Platforms (META 720.37, +2.86, +0.5%).

Large-cap stocks slightly outperformed the broader market.

The Vanguard Mega Cap Growth ETF rose 0.3%, compared to a 0.1% gain in the S&P 500.

Russell 2000 (+0.5%) and S&P Mid Cap 400 (+0.2%) also outperformed the S&P 500.

Seven sectors of the S&P 500 closed higher, with gains ranging from 0.1% to 0.7%.

The energy sector (-1.2%) was the only one to move more than 1%, dragged down by a 2.3% drop in oil prices to $66.90 per barrel.

Treasuries traded in a narrow range, reflecting a general wait-and-see stance ahead of this week's key economic reports. There were no major U.S. economic data releases on Monday.

Energy market

Brent crude fell to $68.60, failing to hold above $70 —a sign of weakness.

Conclusion The outlook remains unchanged—this could still turn into a new leg up or a healthy correction. Much depends on the major bank earnings and today's CPI report. If there's a sharp pullback, we'll be looking for buying opportunities.

*La presente analisi del mercato ha un carattere esclusivamente informativo e non rappresenta una guida per l`effettuazione di una transazione.

Le recensioni analitiche di InstaSpot ti renderanno pienamente consapevole delle tendenze del mercato! Essendo un cliente InstaSpot, ti viene fornito un gran numero di servizi gratuiti per il trading efficiente.