Legenda tim InstaSpot!

Legenda! Anda pikir legenda adalah retorika yang bombastis? Lalu, bagaimana menyebut seorang pria, seorang Asia pertama yang memenangkan kejuaraan catur dunia junior pada usia 18 tahun, dan yang menjadi Grandmaster India pertama pada usia 19 tahun? Itulah awal perjalanan yang sulit dalam meraih gelar Juara Dunia bagi Viswanathan Anand, pria yang menjadi bagian dari sejarah catur untuk selamanya. Sekarang, satu lagi legenda masuk ke dalam tim InstaSpot!

Borussia merupakan salah satu klub sepakbola paling terkenal di Jerman, yang telah berulang kali membuktikan pada para penggemarnya: semangat kompetisi dan kepemimpinan pasti akan mengarah pada kesuksesan. Lakukan trading dengan cara yang sama seperti para profesional olahraga: percaya diri dan aktif. Gunakan "kunci" dari Borussia FC dan jadilah yang terdepan bersama InstaSpot!

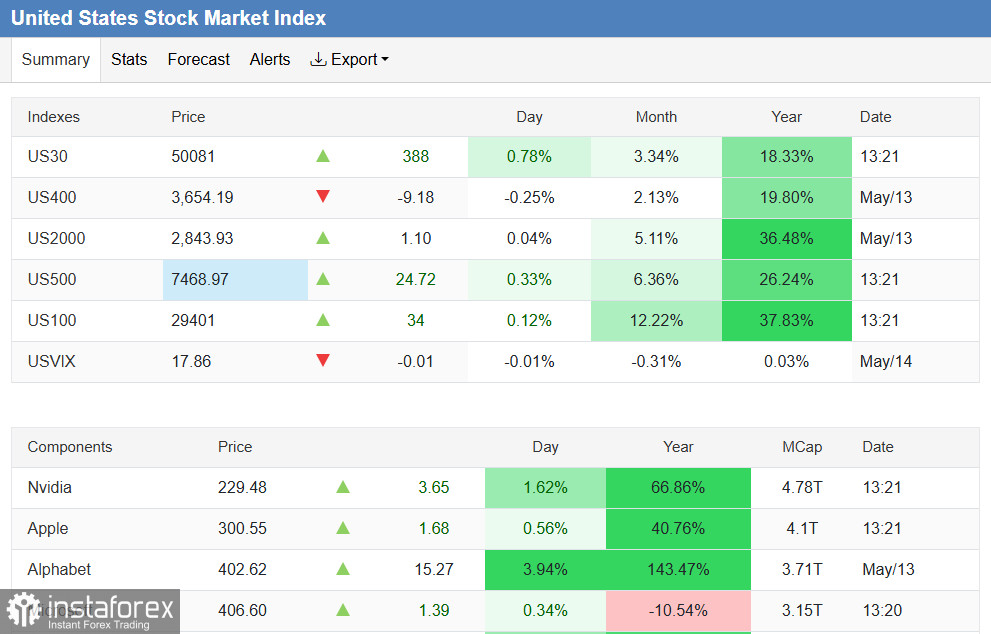

The US equity market continues to show surprising resilience. In the first half of the European session on Thursday, the S&P 500 updated its all-time high, trading above 7,470.00.

This happened despite shocking producer price inflation (PPI) data, which rekindled fears of further monetary tightening. Investors instead leaned on the US-China leaders' meeting, hoping the summit would reduce trade risks, and refocused on the technology sector.

Fundamental backdrop: ignoring reality, a hawkish pause, Warsh's nomination, and the US-China summit

Yesterday, the main source of market jitters was the April producer price index. The figures were shocking and, following Tuesday's CPI release, again pointed to inflation that is not retreating.

Key PPI readings:

- Annual PPI: 6.0%, forecast 4.9%, previous 4.3%

- Core PPI (y/y): 5.2%, forecast 4.3%, previous 4.0%

- Monthly PPI: 1.4%, forecast 0.5%, previous 0.7%

These were the strongest readings since December 2022. What is especially worrying is that the rapid rise in energy prices (driven by the blockade of the Strait of Hormuz) is beginning to spread across sectors, implying a broader pass-through of inflation. Economists warn that the divergence between PPI and CPI has reached its widest levels since 2010, signaling persistent inflationary pressure in the months ahead.

Despite this inflation shock, the market did not plunge into a deep sell-off. That is explained by investors' choice to focus on the US-China summit and a strong technology sector, temporarily abstracting from worrying signals.

Markets immediately repriced expectations, fully ruling out rate cuts in 2026 and shifting the focus toward the possibility of a rate hike by year-end. 30-year Treasury yields approached 5%, increasing the opportunity cost for investors.

The hawkish bias was cemented by the Senate's confirmation on Wednesday of Kevin Warsh as the new Fed chair. His nomination intensifies concerns about prolonged tight policy, as he is known to favor a strong dollar and oppose an easy approach.

The summit between US President Donald Trump and China's President Xi Jinping became the main event preventing a broader sell-off. Expectations of concrete breakthroughs were low, but the meeting itself and signs of stabilizing relations were received positively.

Reports indicate the sides discussed greater access for US firms to the Chinese market and increased Chinese investment. A key outcome was also an assertion that the Strait of Hormuz should remain open and that Iran must never obtain nuclear weapons. That geopolitical statement was a powerful positive signal. The tech sector received an additional boost from the presence of Nvidia CEO Jensen Huang in Trump's delegation, which raised hopes of eased export restrictions.

Brief technical analysis

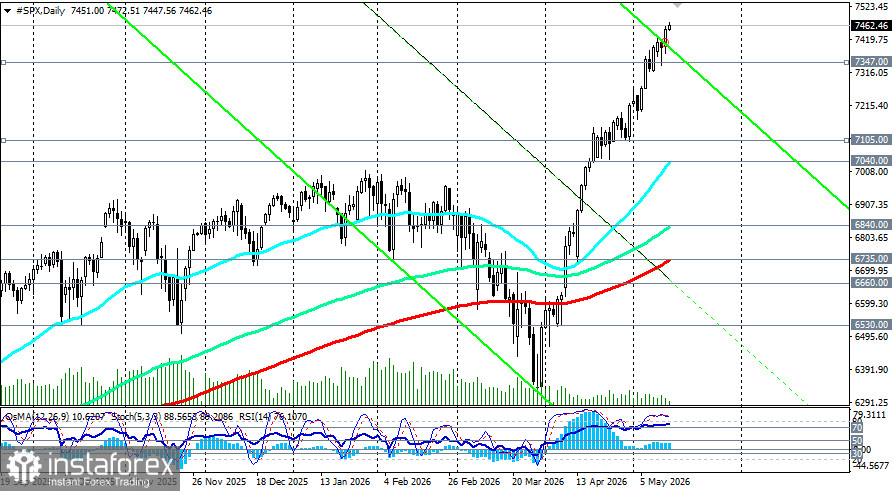

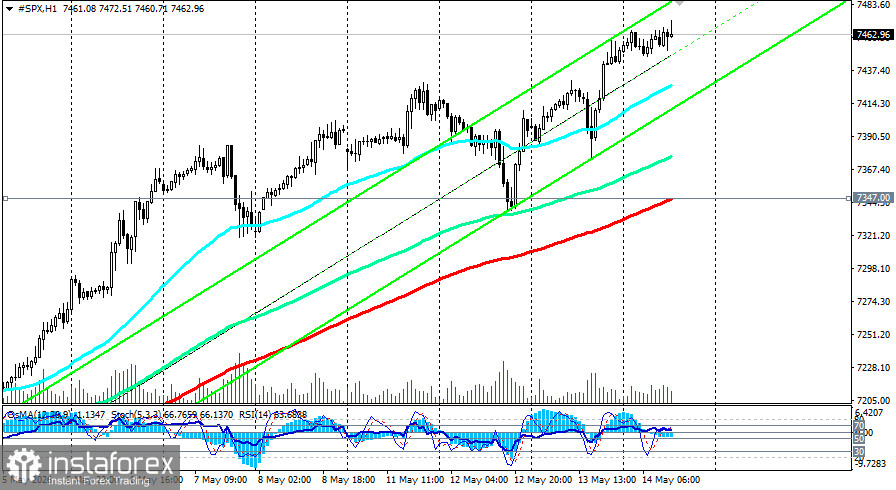

From a technical standpoint, the S&P 500 continues to show strong bullish dynamics after a powerful rebound from lows near 6,310.00 at the end of March.

In short, medium, and long timeframes, price trades above key moving averages (50, 144, and 200), and main indicators remain in bullish territory.

On the daily chart, RSI and stochastic sit in overbought territory, signaling potential consolidation or correction after the extended advance, which is also hinted at by the OsMA histogram. OsMA remains above zero but is no longer increasing and is slightly declining.

The most likely scenario in the coming days is continued consolidation in the 7,400.00–7,500.00 range, with a possible dip to 7,347.00 (EMA200 on the 1-hour chart). The market will digest the summit outcomes and assess the real substance of any trade and technology agreements, which may be less significant than hoped.

Key events

- Thu–Fri, 13–14 May: US President Trump meets China's President Xi Jinping in Beijing — the main geopolitical trigger; any agreement on tech or tariffs would support the rally.

- Today, 12:30 GMT: US retail sales data for April—assessment of consumer demand resilience.

- 15 May: official end of Jerome Powell's term as Fed chair — completion of the Fed leadership transition.

Conclusion

The S&P500 faces a paradoxical situation. Shocking inflation data (annual PPI jumped to 6.0%) and rising expectations of hawkish Fed policy (bond yields are rising) create a classic bearish backdrop. Yet the technology sector, buoyed by hopes of eased China restrictions and resilient corporate profits, continues to drive the index higher.

The key zone 7,400.00–7,500.00 will be the arena of the decisive battle in the coming days. Holding above 7,410.00 preserves the chance to break 7,500.00 and move toward 7,600.00. Technical indicators in overbought territory warn of a possible correction, but for now the summit-driven fundamental impulse remains stronger.

See also: S&P500 (SPX): scenario outlook on 14.05.2026

With inflation continuing to rise, the technology sector remains resilient. That resilience, together with diplomatic hopes in Beijing, has kept the market from falling. Investors should closely watch summit results, retail ales data, and comments from new Fed Chair Kevin Warsh.

*Analisis pasar yang diposting disini dimaksudkan untuk meningkatkan pengetahuan Anda namun tidak untuk memberi instruksi trading.

Tinjauan analitis InstaSpot akan membuat Anda menyadari sepenuhnya tren pasar! Sebagai klien InstaSpot, Anda dilengkapi dengan sejumlah besar layanan gratis untuk trading yang efisien.