Borussia is one of the most titled football clubs in Germany, which has repeatedly proved to fans: the spirit of competition and leadership will certainly lead to success. Trade in the same way that sports professionals play the game: confidently and actively. Keep a "pass" from Borussia FC and be in the lead with InstaSpot!

Naš tim čini više od 7.000.000 trgovaca!

Svakog dana zajedno radimo na unapređenju trgovanja. Ostvarujemo vrhunske rezultate i krećemo se samo napred.

Priznatost od strane miliona trgovaca širom sveta najbolje pokazuje koliko se naš rad ceni! Napravili ste svoj izbor i mi ćemo učiniti sve što je neophodno da zadovoljimo vaša očekivanja!

Zajedno činimo sjajan tim!

InstaSpot. Sa ponosom radi za Vas!

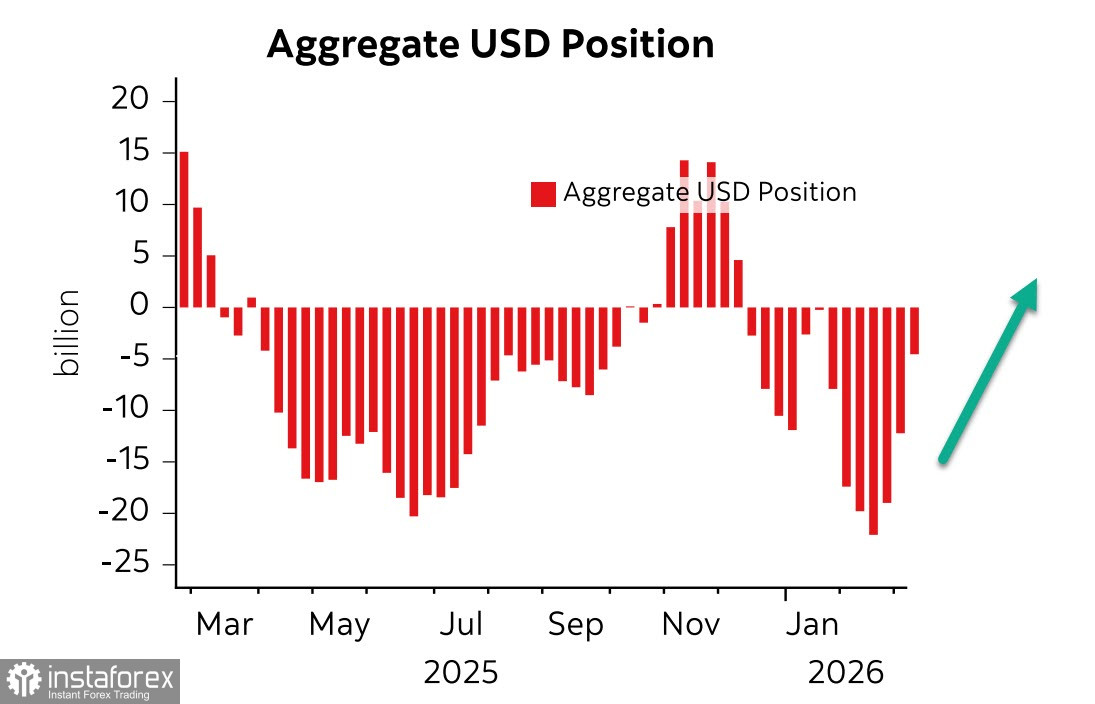

Speculative positioning is rapidly shifting in favor of the US dollar. According to the latest CFTC report, aggregate short dollar positions decreased by $7.5 billion over the week, with almost all the repositioning coming out of the euro and the yen — the two currencies most vulnerable to rising oil and gas prices, since the main energy supply routes to the EU and Japan are tied to the Persian Gulf.

If Japan has little choice, Europe is a textbook case of political folly and energy self-sabotage. Europe voluntarily gave up reliable supplies of cheap energy and simultaneously undermined its own nuclear generation, creating obvious vulnerability.

If the war in the Gulf drags on, the euro's prospects are very poor — and speculators are pricing that in by rapidly trimming long euro exposure.

For now, the market prefers to hope that the conflict will be short and that oil and LNG flows from the Gulf will resume. This is evident in the moderate oil price jump, despite the sharp supply curbs.

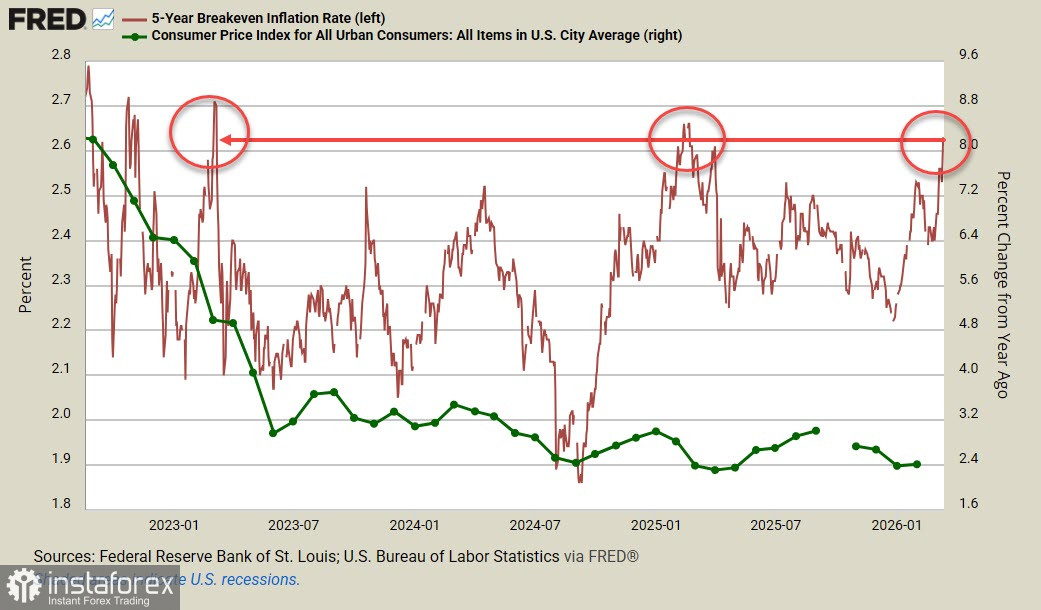

As for the US economic picture, pessimism is already winning out. Q4 GDP was revised down from 1.4% to 0.7%, worsening an already negative picture suggested by very weak labor market reports in recent months. Inflation dynamics remain mixed: core PCE rose by 0.4% in January and by 3.1% year-on-year, 0.1pp higher than in December. Durable goods orders were flat in January, a clear sign of weak consumer demand, while the 5-year TIPS yield is near a three-year high, which means that business sees the risk of further inflation acceleration.

Cooling consumer demand will widen the budget deficit, government debt, and the current account shortfall. In the long run, that poses major problems for the US dollar, and we believe that ultimately it should weaken. The current strength is only a short-term market reaction. A growing current account deficit increases the US economy's dependence on foreign capital, and if equity markets, for example, start to slide from record highs, capital inflows would abate, with the deficit widening further.

A likely slowdown in GDP growth would almost certainly produce such a scenario, and, combined with expected higher inflation, will put both the US government and the Federal Reserve in an even more difficult position. Already, Fed funds futures imply just one rate cut this year — and that only in December — so markets are pricing in a very high inflation threat. That, in turn, points to the prospect of stagflation — the worst-case outcome for any central bank or government.

We assume that the US dollar will remain strong in the short term, until there is credible hope the Gulf war will end. Over the longer term, however, an increasing number of indicators point to its eventual weakening.

*Analiza tržišta koja se ovde nalazi namenjena je boljem razumevanju tržišta i ne pruža instrukcije za vršenje trgovanja.

Uz InstaSpot-ove analitičke preglede uvek ćete biti u toku sa tržišnim trendovima! Klijentima InstaSpot-a su dostupni mnogobrojni besplatni servisi za uspešno trgovanje.