Gold has undoubtedly become the hit of 2020, and many investors have turned their attention to it not only as a safe haven asset but also as an asset that can generate profits by increasing its value. However, where there is massive psychosis in the markets, there is always the possibility of a sharp price movement in the opposite direction, and today I would like to cool off the hotheads who expect the precious metal to rise rapidly to new highs.

Perhaps I will be wrong in my fears, moreover, for many years I have been a supporter of investing in gold, but a reasonable person is always prone to doubts, which makes his choice conscious and more balanced. Therefore, I decided to share my doubts in order to show the reverse side of the coin, and not only the one that blinds the eyes and fogs the mind with its brilliance. All the more so as new input from the World Gold Council brings a healthy dose of pessimism to the optimism in the precious metals markets, but let's start with it.

Against the backdrop of widespread optimism about the prospects for gold prices, there are a number of significant negative aspects and factors affecting the gold price in this market that should be mentioned. As you know, price is a derivative of supply and demand, and the current rise in the price of gold on the market should theoretically be caused either by increased demand or lack of supply. However, is it really so?

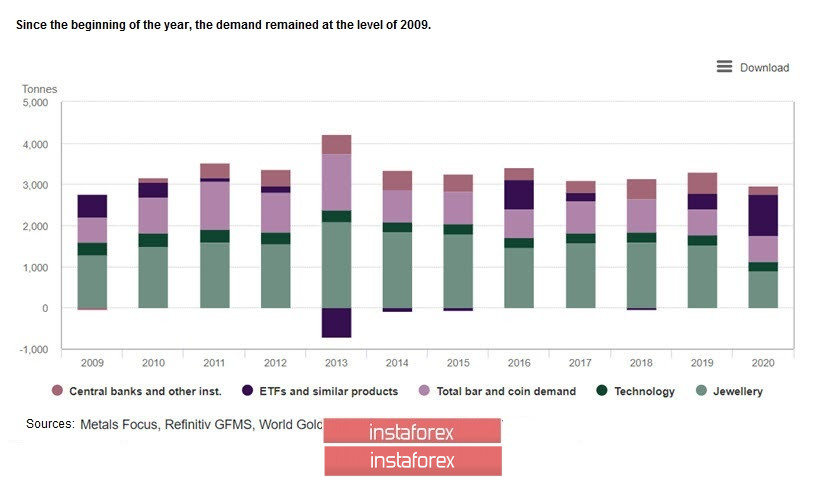

Figure 1: Chart of demand in the gold market from 2009 to 2020

As suggested in Figure 1, the demand for gold in 2020 is at its lowest level since 2009. In other words, buyers in their general mass now do not want to buy gold, which is associated with its high cost, as well as a drop in demand for jewelry, including primarily in India and China. Compared to that of 2019, in 2020, the demand for jewelry in India decreased by 48%, and in China by 25%. The demand for technological use of gold decreased by 6%. In the third quarter of 2020, central banks had negative purchases of gold.

If it were not for the purchase of coins and bars by 49% and investments in exchange-traded funds ETF by 5%, which brought an overall increase of 21%, the demand in the gold market would have collapsed to the minimum values, but this did not happen thanks to investors who believed in gold.

The increase in prices and the decline in supply also helped, which increased to -3% in the third quarter of 2019. However, as the global economy recovers, the supply of gold to the markets will increase. For example, Russia returned to the gold market, which provided the country with a greater inflow of foreign exchange from gold exports than from gas exports. The recovery in production at less profitable mines is accompanied by peaks in the price of gold not only in US dollars, but also in local currencies, which makes mining profitable where production would have been impossible at previous prices, but now it is quite profitable.

As we can see from the data provided by the World Gold Council, the price increase was mainly due to the demand of American and European investors, as well as positioning in the US futures markets. However, as per my previous article published a week ago, the CME has significantly increased the margin for speculators who are a priori net buyers, literally forcing them to leave the market. According to the COT Traders' Commitment Report, as a result of the exchange's actions, long positions of speculators have decreased by more than a third since March 2020, while their total position is minimal, and short positions are maximum since summer 2019.

Thus, based on the data on supply and demand, the following conclusions can be drawn: the recovery in demand for jewelry in India and China, which will occur as the economies of these countries recover, will be accompanied by an increase in supply from the mining industry. However, the position of American investors, who currently provide the main price driver, may change after the US elections, for example, due to the growth of the US dollar.

Now, most forecasts assume that the stock market will decline, and gold will simultaneously serve as a safe-haven asset and as an inflation-defender asset. At the same time, the decline in stock markets is always accompanied by a contraction of liquidity, when the dollar rises in price in relation to all assets, including gold. Moreover, the period between the beginning of a decline and an increase in the price of gold can reach several quarters.

However, even if we assume that the US stock market does not collapse, but remains in the range or even continues to grow, will gold become as desirable an asset for investors as it was in 2020? If American investors turn their backs on gold, it will simply collapse, and it will collapse quite deeply.

On Friday, gold is above the substantial support of 1854, but it has already dipped to the half-year averages. On the one hand, this indicates the weakness of the market in the medium term, and on the other hand, it accurately describes the current situation (Fig. 2), which, in the event of a decline in the price of gold, suggests targets at $ 1750, $ 1680, and $ 1500 per troy ounce. To be honest, I don't think gold buyers who bought it at $ 2,000 would be happy that the price dropped to the 1,500 mark.

Figure 2: Medium-term outlook for gold is negative

If on top of everything else, the US dollar starts strengthening against a basket of foreign currencies and, first of all, against the euro on the market, then gold will begin to actively lose its price. Moreover, the strengthening of the dollar can occur not only in the event of a decline in stock markets but also in the event of their growth. The dollar and stock markets do not have a direct correlation.

Here are just a few reasons why the dollar might rise as equity markets rise. The situation in the US is better in terms of interest rates than in Europe. The US economy is more adapted to the shock of the COVID-19 pandemic than the eurozone economy, which, in addition to the coronavirus pandemic, is experiencing a painful divorce from the UK. The dollar is also the dollar in Africa, and all other things being equal, investors will choose it. Why not assume in this regard that the dollar has the potential to strengthen by 10% against the euro?

Summing up my reflections, I would especially like to draw the readers' attention to the fact that I am not calling for the complete liquidation of gold-bearing assets in portfolios, but talking about a possible scenario and a revision of views on gold as an asset that will always grow in price. I also draw the attention of traders to the possibility of selling gold in the medium term, but only if their trading systems generate appropriate signals. However, I remind you that selling against the current long-term trend is always an action against the expected value and often leads to losses, so be careful and make sure to follow the rules of capital management.

*تعینات کیا مراد ہے مارکیٹ کے تجزیات یہاں ارسال کیے جاتے ہیں جس کا مقصد آپ کی بیداری بڑھانا ہے، لیکن تجارت کرنے کے لئے ہدایات دینا نہیں.

InstaSpot analytical reviews will make you fully aware of market trends! Being an InstaSpot client, you are provided with a large number of free services for efficient trading.