La légende dans l'équipe InstaSpot!

La vraie légende! Vous pensez que c'est trop pathétique? Mais comment pouvez-vous appeler un homme qui, à 18 ans, est devenu le premier champion du monde d'échecs parmi les jeunes hommes d'Asie, et à dix-neuf ans – le premier grand maître de l'histoire de son pays? Ce fut le début de la voie du champion d'échecs –Viswanathan Anand – l'homme qui a inscrit son nom à jamais dans l'histoire des échecs du monde. Une autre légende dans l'équipe d'InstaSpot!

Le FC Borussia est l'un des clubs de football les plus titrés d'Allemagne, qui a prouvé à maintes reprises à ses fans que l'esprit de rivalité et de leadership mènera certainement au succès. Négociez de la même manière que les professionnels du sport mènent le jeu: en toute confiance et activement. Devenez un leader avec le FC Borussia et soyez en tête avec l'équipe InstaSpot!

It's time for the Bank of Japan to rid itself of ultra-loose monetary policy. Not only has inflation exceeded the 2% target for the 19th consecutive month, but the losses from the BoJ's balance sheet bonds from April to September have surged to £10.5 trillion. This is equivalent to $70.7 billion, more than six times the losses for the entire 2022/2023 fiscal year. While this alone won't make Kazuo Ueda abandon negative rate policies, it can be used as one of the arguments, which is good news for USD/JPY bears.

It can't be said that the new head of the Bank of Japan is sitting idle. Under his leadership, the range of the targeted yield for 10-year bonds was expanded to 1%, and its boundaries became flexible. Getting rid of the legacy of the past is in progress. However, if this process is accelerated, it could harm both the domestic economy and financial markets.

Japan is known to be the largest holder of U.S. Treasury bonds. If the BoJ begins to normalize monetary policy, there is a significant risk of capital repatriation to Asia, pushing bond yields higher and exerting pressure on the global economy. Japanese banks, insurance companies, and pension funds reduced their holdings of U.S. bonds to $550 billion by the end of 2022, compared to $840 billion two years prior. In 2023, the process was restrained by a weak yen, but in 2024, it risks accelerating.

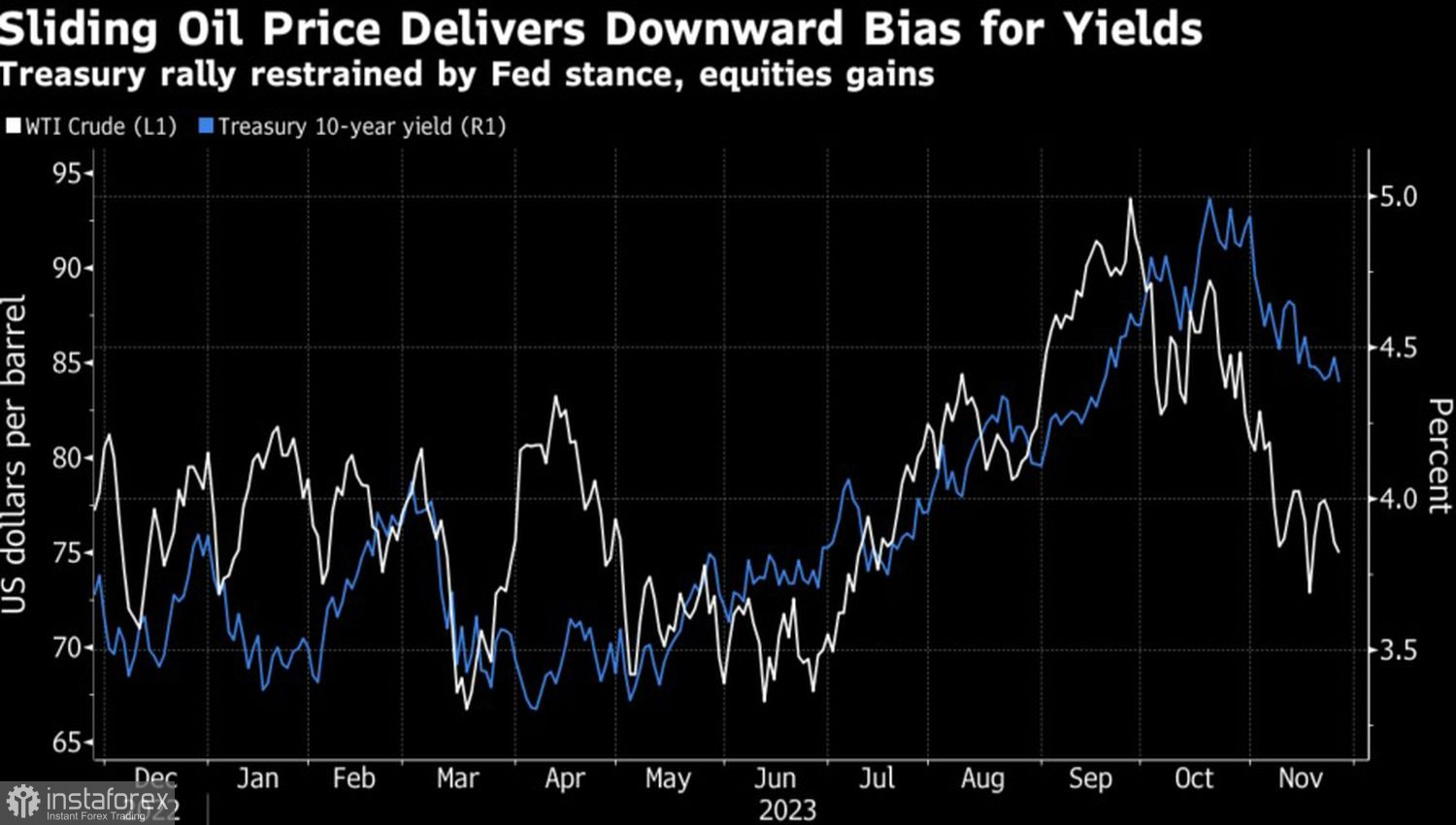

The slowdown in U.S. inflation gives markets grounds to predict a 100 basis point rate cut to 4.5% in federal funds. This leads to a decline in bond yields and the U.S. dollar. At the same time, a roughly 20% drop in oil prices from September highs can accelerate this process.

Dynamics of U.S. bond yields and oil prices

So, USD/JPY bears will benefit twice. As an energy-importing country, Japan benefits from falling oil prices. Simultaneously, the reduction in U.S. Treasury yields narrows the spread with their Japanese counterparts and strengthens the yen against the U.S. dollar.

The basis for this process is the divergence in monetary policy between the Fed and BoJ. If Ueda has no choice but to gradually abandon targeting the yield curve, negative rates, and QE, then Jerome Powell and his team must consider the need to ease monetary policy. The divergence between the U.S. and Japan could make the yen the main favorite in the Forex market in 2024.

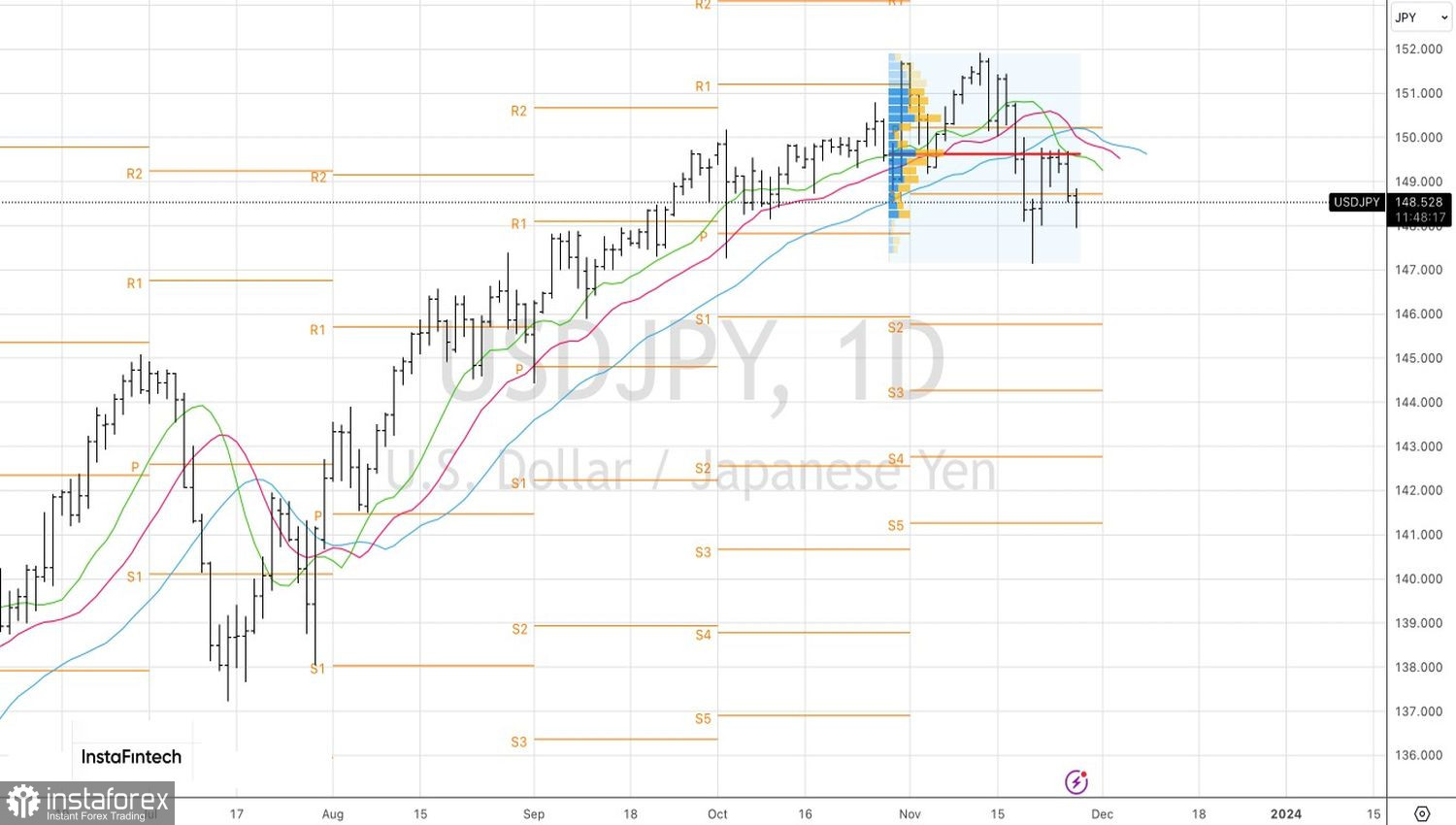

Technically, on the daily chart of USD/JPY, bulls are trying to prove themselves. The formation of two consecutive pin bars within the 1-2-3 pattern is a strong reversal formation. Therefore, a confident assault on the fair value at 149.65 could be the basis for buying. However, it may not come to that, so we continue to sell the dollar towards 146.0 and 142.5.

*The market analysis posted here is meant to increase your awareness, but not to give instructions to make a trade.

InstaSpot analytical reviews will make you fully aware of market trends! Being an InstaSpot client, you are provided with a large number of free services for efficient trading.