The legend in the InstaSpot team!

Legend! You think that's bombastic rhetoric? But how should we call a man, who became the first Asian to win the junior world chess championship at 18 and who became the first Indian Grandmaster at 19? That was the start of a hard path to the World Champion title for Viswanathan Anand, the man who became a part of history of chess forever. Now one more legend in the InstaSpot team!

Borussia is one of the most titled football clubs in Germany, which has repeatedly proved to fans: the spirit of competition and leadership will certainly lead to success. Trade in the same way that sports professionals play the game: confidently and actively. Keep a "pass" from Borussia FC and be in the lead with InstaSpot!

The markets were overwhelmed by a wave of enthusiasm again. The rise in energy prices is explained not so much by management errors as by growing demand, and as already known, demand has a direct connection with economic activity. The increase in inflation in most countries of the world is also considered a positive sign indicating growing consumer demand, and not at all a dangerous trend of the overflow of support programs issued over a year and a half during an undeclared pandemic into the consumer sector.

The VIX volatility index continues to decline and is already near the dock lows. The first corporate reports are positive, which supports the growth of stock indices. Yields continue to grow across the entire spectrum of the market.

But is everything so good?

The UK's inflation fell from 3.2% to 3.1% in September. Core inflation also slightly decreased from 3.0% to 2.9%. The pound reacted with a temporary decline, and by the end of the day, the pound fully recovered its position. Markets did not see the decline in consumer prices as a sign of a long-term trend.

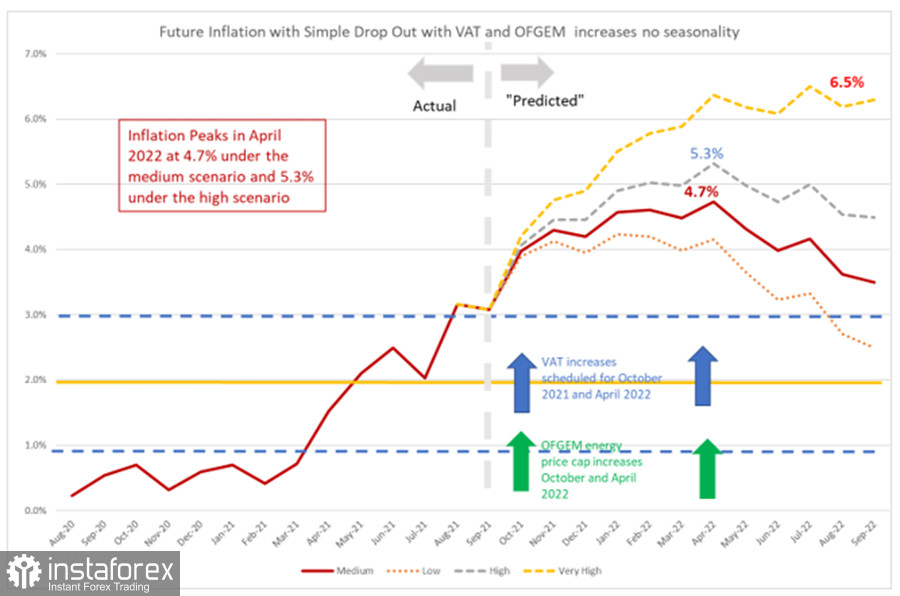

The NIESR Institute conducted a small study in order to find out what factors influence the dynamics of consumer prices in the coming year. Even under the weakest "low" scenario, assuming that inflation will increase by only 1% y/y each month, it will remain above 4% until April 2022. Meanwhile, other more realistic scenarios said that it will be in the range of 4.7%-6.5%.

NIESR believes that a high level of inflation will be implemented if the problems with supply chains and energy carriers persist (do not even worsen), and if so, it will mean a complete failure of the Bank of England's inflation targeting policy. This, in turn, will mean a loss of trust.

It is necessary to stop inflation, which is a strategic issue, hence the forecast that the Bank of England will raise the rate already in November by 0.15% (which will have only symbolic significance and will not have a serious impact on financial conditions). The demand for the pound is due to expectations of a rate hike, but the pace that the market assumes, based on the expected increase in inflation, will be very difficult for the UK economy. Therefore, the demand for the pound has currently no fundamental justification.

It is assumed that the pound will continue its short-term growth in anticipation of the BoE meeting. The border of the channel 1.3820/40 has been reached, so a pullback to 1.3740/50 is technically possible, which will be used for purchases. The target of 1.3900/20 is relevant, but sharp long-term growth is questionable.

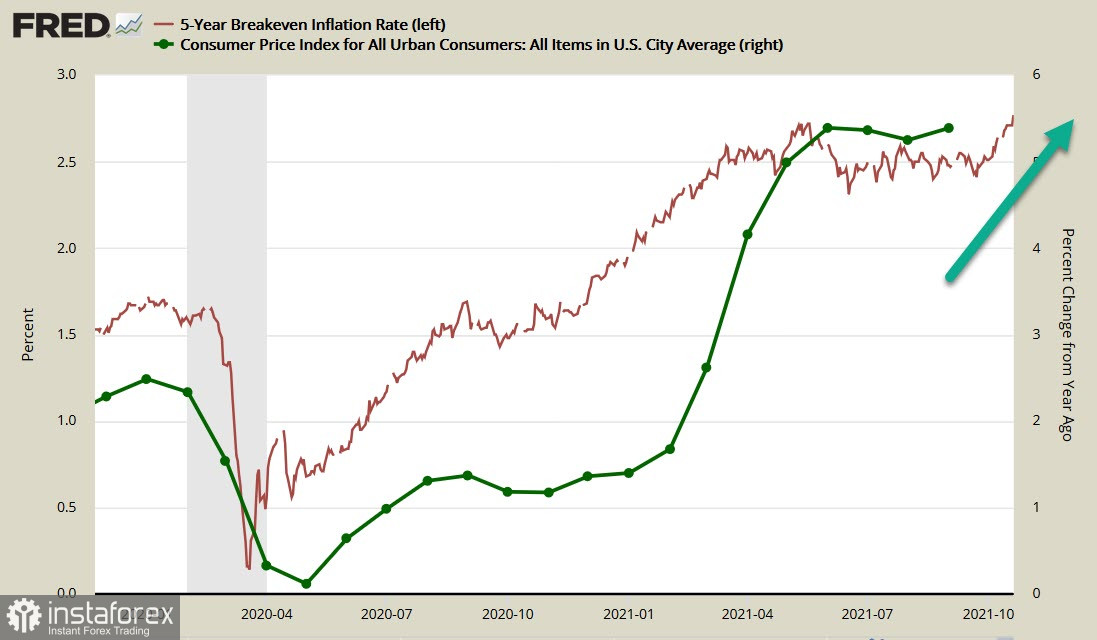

Meanwhile, the yield of 5-year Tips bonds reached 2.77%, and this is the maximum since March 2005. It can be argued that inflation expectations in the US are growing and attempts to declare this growth temporary has no serious grounds.

The growth of inflation around the world is quite clear. Following the Bank of England and the RBNZ, Scotiabank predicts that the Bank of Canada will begin to raise the rate, with an increase of at least 1% expected in 2022. In turn, the Fed is only going to reduce QE programs for now, but if the inflation growth does not stop, then the rate forecasts will also have to be revised.

The current trends are viewed by the markets as temporarily positive, so the growth in demand for risky currencies will continue. The winners will be AUD, CAD, and NZD. As for the yen, franc and euro, the situation is much worse. The chances of their growth until the end of the era of energy scarcity are minimal, and this is unlikely to happen before March-April. December Brent futures tested the level of $ 86/barrel, and since OPEC+ is determined to adhere to the production growth schedule, oil prices can only change in the direction of growth until the end of the year. The winter will be hot, even if it turns out to be very cold.

*这里的市场分析是为了增加您对市场的了解,而不是给出交易的指示。

InstaSpot分析评论将让您充分了解市场趋势! 作为InstaSpot的客户,您将获得大量的免费服务以实现有效的交易。