The legend in the InstaSpot team!

Legend! You think that's bombastic rhetoric? But how should we call a man, who became the first Asian to win the junior world chess championship at 18 and who became the first Indian Grandmaster at 19? That was the start of a hard path to the World Champion title for Viswanathan Anand, the man who became a part of history of chess forever. Now one more legend in the InstaSpot team!

Borussia is one of the most titled football clubs in Germany, which has repeatedly proved to fans: the spirit of competition and leadership will certainly lead to success. Trade in the same way that sports professionals play the game: confidently and actively. Keep a "pass" from Borussia FC and be in the lead with InstaSpot!

Yesterday, equity indices finished lower. The S&P 500 fell by 0.74%, and the Nasdaq 100 dropped by 0.89%. The Dow Jones Industrial Average lost 1.21%.

The record rally stumbled on two fronts — and both hit on the same day. A weak guide from Broadcom dented the AI narrative, and renewed clashes between the US and Iran knocked the wind out of sentiment. The MSCI Asia Pacific index fell by 1.6%, ending a four-day run to record highs. South Korea's KOSPI, the world's best-performing index this year, lost 1.7%. Nasdaq 100 futures were down about 0.5%. The S&P 500 ended a nine-day winning streak. Europe is set to open lower.

As noted earlier, Broadcom was the day's main disappointment. The stock plunged by about 14% in after-hours trade after a guidance miss and management commentary that the shift toward AI customers is progressing more slowly than expected. One weak guide from one company is not automatically a trend reversal. Still, after such a rapid run in chip names — the Philadelphia Semiconductor Index has gained roughly 70% in two months — investors need little reason to start taking profits.

Geopolitics added pressure. Renewed US–Iran clashes returned familiar nervousness to markets. Brent is trading near $97/bbl, though a US announcement of a ceasefire between Israel and Lebanon briefly eased tensions and helped oil pull back nearly 1%. Bitcoin slid below $62,000, a low not seen since February.

Labor market data continue to surprise on the upside. Yesterday's ADP report showed that US firms added the most jobs since January 2025. This indicates that hiring remains resilient despite the energy shock. Friday's nonfarm payrolls data remains the week's main event. If the print confirms labor market strength, as preliminary indicators suggest, the Fed will have another argument for holding or raising interest rates. That's constructive for the dollar and negative for gold and supportive for the yen.

Meanwhile, Dallas Fed President Lorie Logan said that a return of inflation to the target level may require interest rate hikes later in the year. New York Fed President John Williams added caution, calling the outlook for rates "uncertain" — but the market is clearly hearing more hawkish voices than doves.

In the foreign exchange market, the yen unexpectedly strengthened today. According to reports, the Bank of Japan is considering a 25bp rate hike this month with more tightening possible toward year-end. That would be a major signal for currency markets: the yen has long been a victim of the global high-rate cycle, and any hint of normalization in Japanese policy could sharply alter the USD/JPY dynamic.

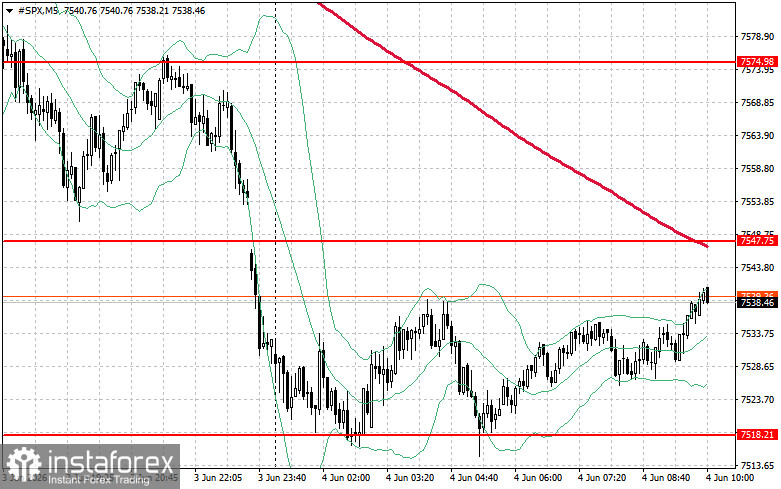

Technically, the S&P 500 analysis suggests that the immediate task for buyers is to overcome the resistance level of $7,547. Doing so would confirm upside and open the path to $7,574. Maintaining control above $7,607 would further strengthen buyers' positions. On the downside, buyers need to defend $7,518. A break below that level would likely push the index back to $7,494 and open the way to $7,474.

*Analiza tržišta koja se ovde nalazi namenjena je boljem razumevanju tržišta i ne pruža instrukcije za vršenje trgovanja.

Uz InstaSpot-ove analitičke preglede uvek ćete biti u toku sa tržišnim trendovima! Klijentima InstaSpot-a su dostupni mnogobrojni besplatni servisi za uspešno trgovanje.