A lenda da equipe InstaSpot!

Lenda! Você acha que isso é retórica bombástica? Mas como devemos chamar um homem que se tornou o primeiro asiático a vencer o campeonato mundial de xadrez aos 18 anos e que se tornou o primeiro grande mestre indiano aos 19? Esse foi o começo de um caminho difícil para o título de campeão do mundo para Viswanathan Anand, o homem que se tornou parte da história do xadrez para sempre. Agora mais uma lenda na equipe InstaSpot!

O Borussia é um dos clubes de futebol com mais títulos da Alemanha, que provou repetidamente aos fãs: o espírito de competição e liderança certamente levará ao sucesso. Negocie da mesma maneira que os profissionais do esporte jogam: com confiança e ativamente. Mantenha o "ritmo" do Borussia FC e esteja na liderança com a InstaSpot!

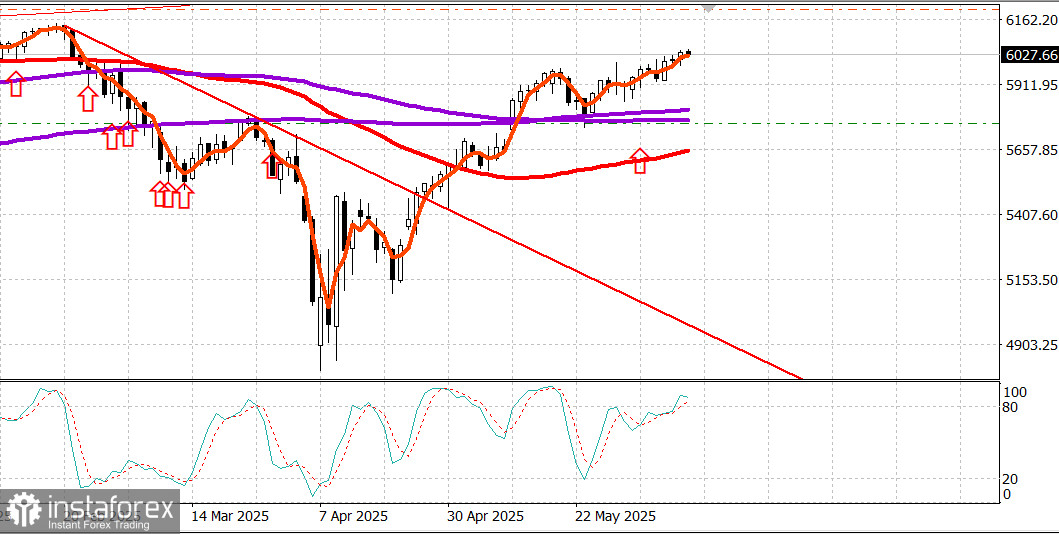

S&P500

Snapshot of major US stock indexes on Tuesday: Dow +0.3%, NASDAQ +0.6%, S&P 500 +0.6%, S&P 500 at 6,038, range 5,400–6,200.

The stock market rose on Tuesday, supported by persistent hopes for a positive outcome in trade negotiations between US and Chinese officials.

The S&P 500 (+0.6%) and the Nasdaq closed with a 0.6% gain each, while the Dow (+0.3%) continued to lag for the month.

The trading session was generally uneventful, although the market resisted two rounds of selling pressure that briefly pulled the major averages off their highs before rebounding to intraday highs again.

President Trump's acknowledgment that Iran is becoming "much more aggressive" in its nuclear talks with the US triggered a brief dip in mid-morning, but this quickly gave way to renewed gains.

Later in the day, Commerce Secretary Lutnick stated that negotiations with China are going very well and may continue tomorrow.

Ten sectors finished the day higher, led by energy (+1.8%), although crude oil failed to hold its morning gains and ended the session down 0.5% at $64.96 per barrel. Consumer discretionary (+1.2%) followed, supported by the continuation of yesterday's rebound in Tesla (TSLA 326.09, +17.51, +5.7%).

The heavyweight technology sector (+0.5%) kept pace with the broader market, bolstered by strength among semiconductor manufacturers. This helped the PHLX Semiconductor Index (+2.1%) extend its monthly gain to 10.2%, with Intel (INTC 22.11, +1.63, +8.0%) showing relative strength amid growing optimism about its new manufacturing technology.

The industrial sector (-0.4%) underperformed due to profit-taking in defense stocks following recent strength.

Transportation stocks performed well, with the Dow Jones Transportation Average (+1.3%) returning to its May high after Norfolk Southern (NSC 252.92, +2.35, +0.9%) reported a 5% quarter-to-date increase in rail volume.

Treasuries ended the day slightly higher at the longer end and modestly lower overall ahead of tomorrow's release of the May Consumer Price Index (consensus +0.2%). The Treasury auctioned $58 billion in 3-year notes in response to weak demand, while tomorrow's session will include a $39 billion reopening of 10-year notes.

The only report worthy of note in the economic calendar was the NFIB Small Business Optimism Index for May, which grew to 98.8 from 95.8 in April.

The economic calendar on Wednesday: At 7:00 AM ET, the market will get to know the MBA Weekly Mortgage Applications Index (previous -3.9%). At 8:30 AM ET, the CPI data for May will be released (consensus +0.2%; previous +0.2%), along with Core CPI (consensus +0.3%; previous +0.2%). At 2:00 PM ET, the Treasury Budget for May will be available (previous -$258.4 billion).

Year-to-date performance of benchmark stock indices

Energy market Brent crude is now trading at $67 a barrel.

Conclusion The stock market continues to creep higher, albeit very slowly. All eyes are on today's inflation reports. For now, we expect further growth.

*A análise de mercado aqui postada destina-se a aumentar o seu conhecimento, mas não dar instruções para fazer uma negociação.

InstaSpot analytical reviews will make you fully aware of market trends! Being an InstaSpot client, you are provided with a large number of free services for efficient trading.