A very tense trading week is drawing to a close. It featured major events linked both to the military confrontation involving the United States and Israel on the one side and Iran on the other and to policy meetings of five of the world's largest central banks, including the Federal Reserve.

Next week will be the final full trading week of the month, quarter, and half-year. Unexpected moves related to portfolio rebalancing cannot be ruled out.

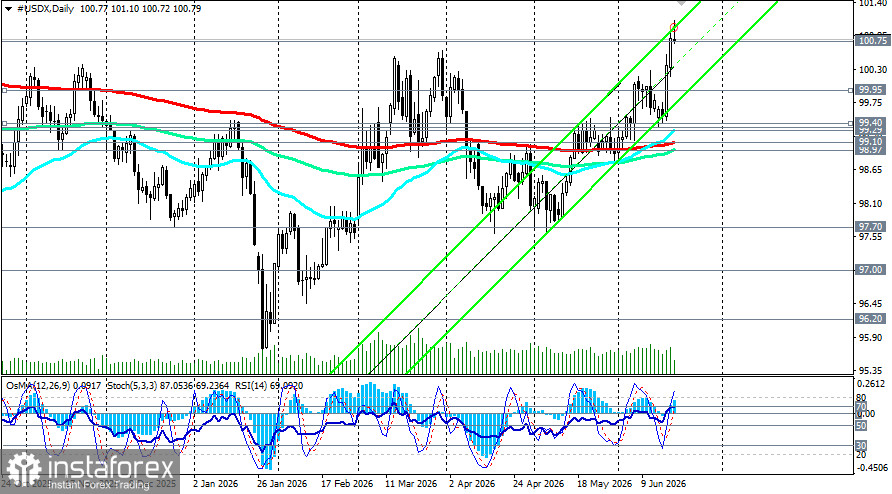

The US dollar index ends the week on a strong note, posting new annual highs and testing the 101.00 area for the first time since May 2025. The primary driver of the rally was a hawkish signal from the Federal Reserve that outweighed even the market impact of a signed framework agreement between the United States and Iran.

On Friday, the index pulled back slightly from a peak of 101.10 but is holding firmly near the key resistance area of 100.75. Markets, trading in reduced liquidity ahead of the US Juneteenth holiday, are digesting a new monetary landscape in which the probability of a Fed rate hike by year-end is assessed at nearly 90%.

The critical question for the dollar next week is whether it can hold the positions it has won or whether geopolitical risks and a correction in yields will return the index to more familiar levels.

Fundamental backdrop: Fed's hawkish signal is dollar's main trump card

1. FOMC: a rhetoric shift and the dot plot

The FOMC meeting on 16–17 June represented an inflection point that materially altered positioning in currency markets. As expected, the Fed held the policy rate at 3.50–3.75% for the fourth consecutive meeting; the decision was unanimous for the first time in nine months. The decisive event, however, was the updated dot plot and the rhetoric of new Chair Kevin Warsh, which proved considerably more hawkish than the market had anticipated.

Key forecast changes

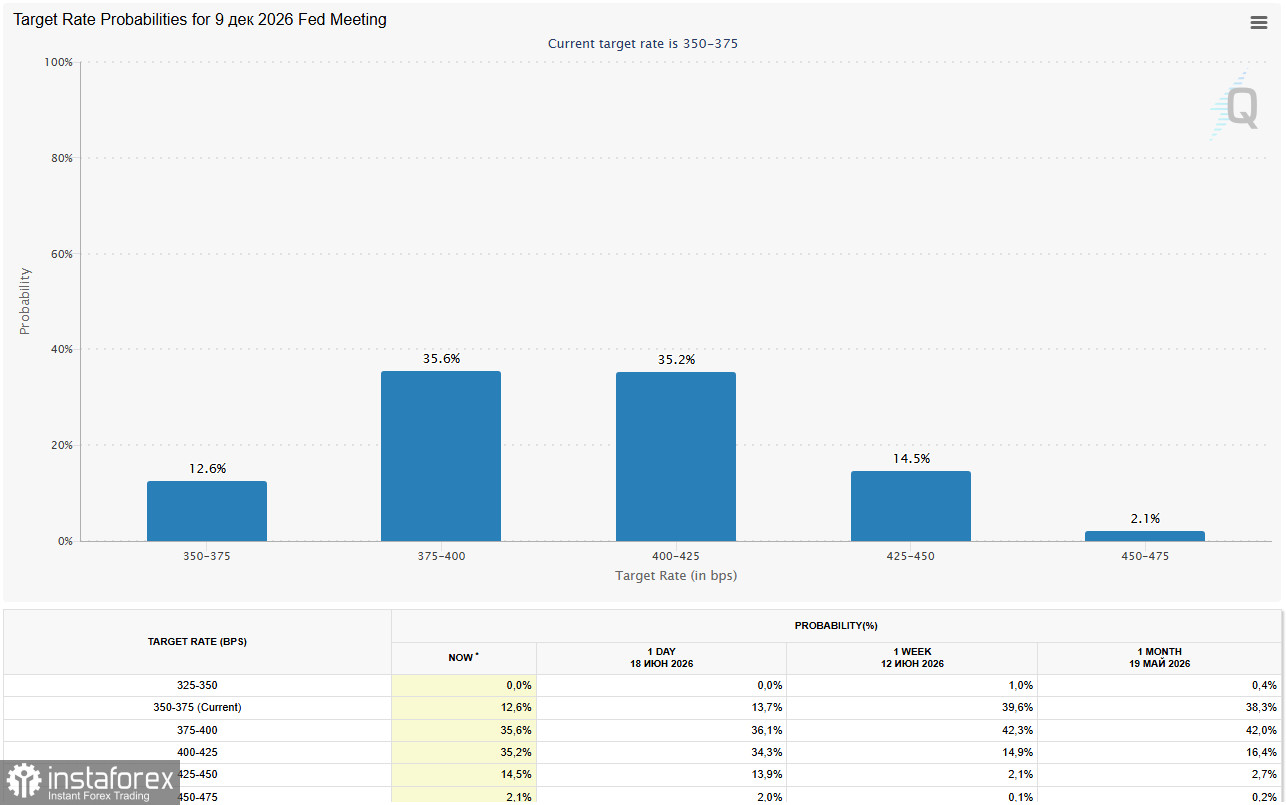

- Dot-plot shift. The median projection for the terminal rate in 2026 was raised to 3.8%. That implies nine of 18 FOMC participants now expect at least one 25-basis-point hike before year-end, and six of them expect two or more hikes. By contrast, only one official still sees rate cuts this year.

- Upward revision to inflation forecasts. Expectations for inflation in 2026 were raised: core PCE was revised to 3.3% and headline PCE to 3.6%.

- Removal of easing language. The statement's formulation that previously hinted at easing as the next step was removed entirely. That represented a clear market signal that the Fed no longer treats cuts as the baseline scenario.

Market reaction to Fed signal

Markets priced rapidly for a rate increase by October or November. The probability of a hike in December is now assessed at 88 percent, and chances of a move by October rose from 40% to 77% in a single week. Two-year Treasury yields, which are sensitive to policy, rose 16 basis points to 4.21%—the highest since February 2025—generating the largest one-day dollar gain since early March.

2. Monetary divergence: why USDX is above 100.00

The dollar's resilience is primarily due to the yield differential in favor of the United States. While the Fed signals the possibility of further tightening, other central banks are in very different positions.

Central bank actions this week and key signals

- Fed: held 3.50–3.75%—a hawkish signal of possible further tightening in 2026.

- ECB: hiked 25 bp to 2.40%—moderately hawkish, but an isolated move.

- BoE: held at 3.75%—a pause, with a small hawkish minority (two votes for a hike).

- BoJ: raised the policy rate to 1.00%—a historic step, but the US-Japan spread remains wide.

- SNB: held at 0%—neutral, emphasis on intervention policy.

The Fed's hawkish update threatens to trigger a sustained dollar advance, more than offsetting the dampening effect of the US-Iran deal, economists say. The United States' growth advantage, underpinned by AI investment and a resilient labor market, continues to attract global capital.

3. Geopolitics: USD weakness is short-lived.

Hopes for a framework agreement between the United States and Iran and the reopening of the Strait of Hormuz pushed oil prices lower and briefly improved global risk appetite, which put short-term pressure on the dollar as a safe haven. But the Fed's hawkish shift outweighed that factor.

Moreover, the Middle East remains unstable. On Friday, Switzerland's foreign ministry said planned talks between the United States and Iran would not go ahead. Israeli strikes in Lebanon and the cancellation of Vice President J.D. Vance's trip to negotiate with Iran add new risks. A renewed escalation could again boost demand for the dollar as a refuge and add another bullish argument for the currency.

Brief technical analysis

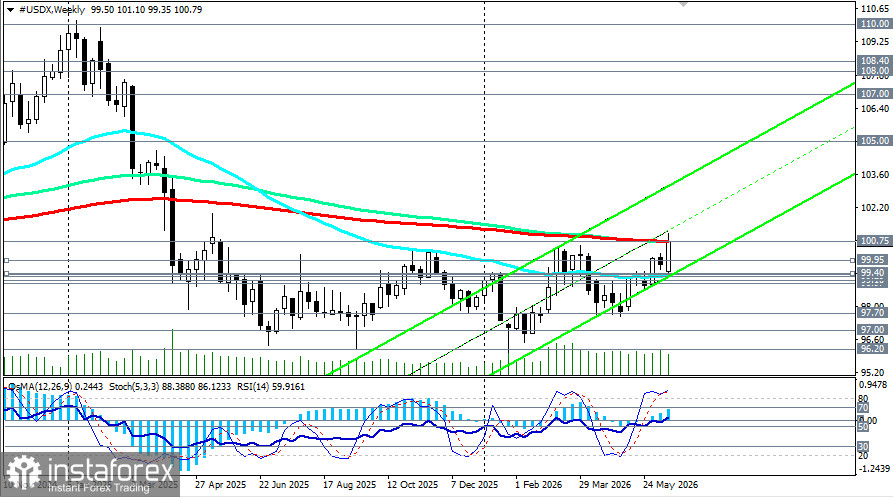

Technically, USDX has confirmed a mid-term trend shift, breaking key resistances at 98.97, 99.10, and 99.29 (the 144-, 200-, and 50-day EMAs) and this week reached an annual high of 101.10. Despite a correction on Friday, the index is holding near the key resistance at 100.75 (the weekly 200- and 144-day EMAs and the monthly 50-day EMA).

The index gained about 1 percent on the week, the best weekly performance since early March. It also remains above short-term moving averages (5, 10, and 20), grouped around 100.71–100.75, indicating the current retracement is being treated as a correction within an uptrend. A technical break above 100.00 and the update of annual highs confirm the resumption of the bull trend. Economists say the move higher was driven by a recalibration of Fed policy and has scope to continue.

For more details, view "US Dollar Index (USDX): possible dynamic for June 19, 2026."

Forecasts from major banks

- Deutsche Bank: year-end EUR/USD forecast 1.1500, implying continued dollar strength.

- Societe Generale: year-end USDX forecast 98.60–99.00, suggesting moderate dollar weakening in H2 but not a structural shift.

- MUFG: sees upside risks to its 2027 dollar weakening scenario, acknowledging that the Fed's hawkish signal creates upward pressure.

Key events to watch next week

- 22 June — PBoC LPR decision: expected unchanged; indirect impact via USD/CNH.

- 22 June — Canadian inflation (May): impact on USD/CAD.

- 23 June — preliminary S&P Global PMIs for Germany, the euro area, and the US: will show divergence in economic momentum.

- 25 June — US PCE (May): expected to remain elevated; a strong print would reinforce the Fed's hawkish stance.

- During the week — Fed speakers: any hawkish comments could strengthen the US dollar.

Conclusion

The US dollar ends the week as the clear outperformer, confirming its strength after the Fed's hawkish surprise. Chair Kevin Warsh's willingness to tighten policy and the dot-plot revision have fundamentally changed market expectations, prompting pricing of possible rate increases by year-end. The dollar benefits both from the interest rate differential and as a safe haven amid persistent geopolitical uncertainty in the Middle East.

The 100.50–101.10 zone will be the decisive battleground in the coming days. A technical break above it would open the path to new multi-year highs, while a sustained close below 100.50 could trigger a correction toward 100.00 and 99.95.

*यहां पर लिखा गया बाजार विश्लेषण आपकी जागरूकता बढ़ाने के लिए किया है, लेकिन व्यापार करने के लिए निर्देश देने के लिए नहीं |

InstaSpot analytical reviews will make you fully aware of market trends! Being an InstaSpot client, you are provided with a large number of free services for efficient trading.